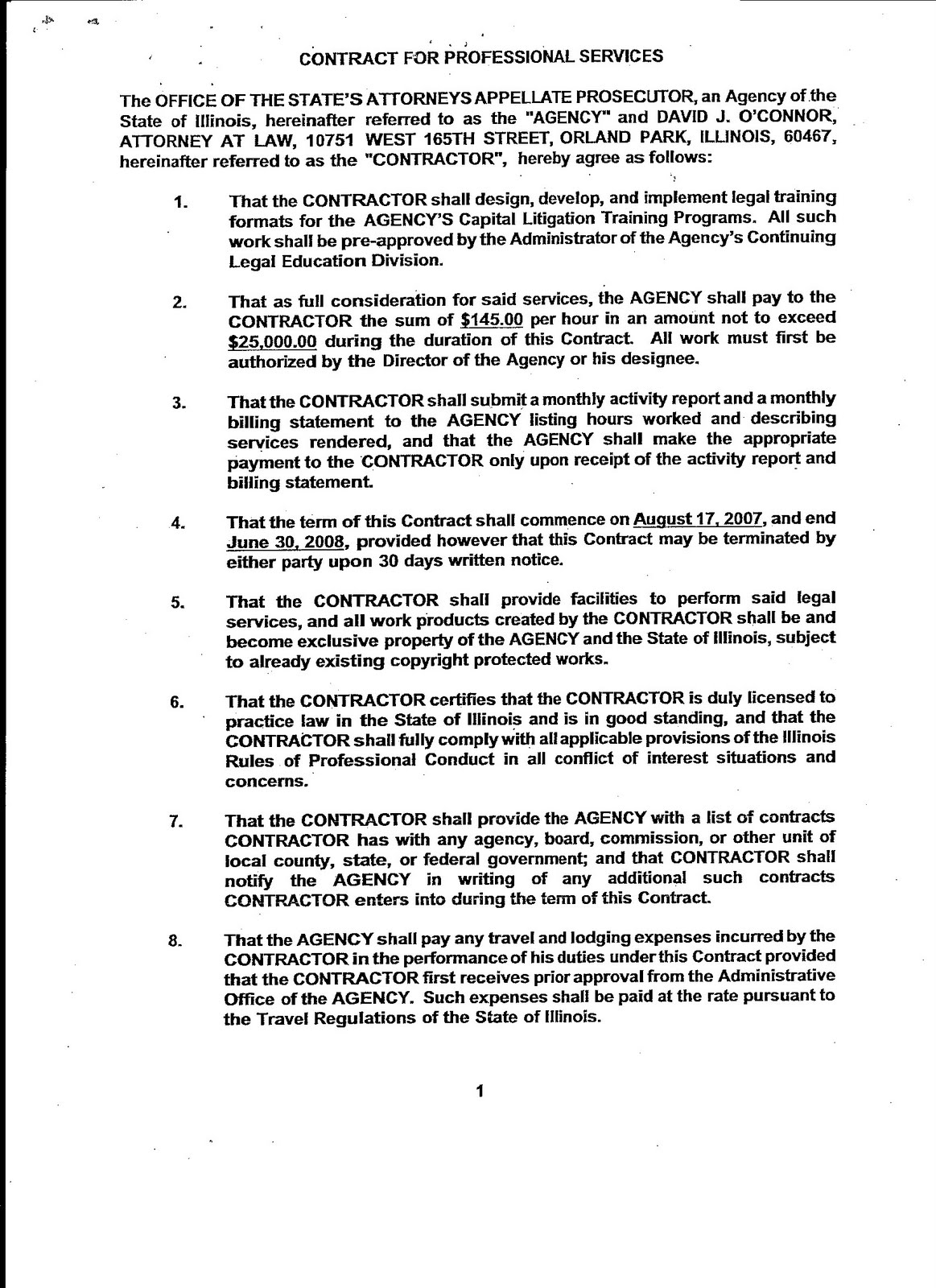

The current rule requires that a CPA, attorney, or enrolled agent rendering tax services, "shall exercise due diligence: (a) In preparing or assisting in the preparation of, approving, and filing returns, documents, affidavits, and other papers relating to IRS matters;

Full Answer

What is tax due diligence when buying a company?

Tax due diligence is a central component of a business transaction. It is important to identify the tax risks and facts that affect the business and its purchase price. If you take over a company, you can save a lot of tax with a well-chosen deal structure.

Is there a tax due diligence template for M&A?

Having provided a due diligence software for hundreds of transactions, DealRoom has been able to put together a template for tax due diligence that addresses all of the tax issues you’re likely to encounter in your M&A process that can be accessed here. The following represents a checklist for US-based companies.

What is the Order of due diligence?

The order of due diligence can change, new stages and procedures include depending on the activity of the company. Most commonly, the procedure goes in this order: 1) Analysis of the legal and corporate structure. This stage identifies the presence of a foreign element in the ownership structure, branches and representative offices.

Why might you seek the help of a tax attorney rather than a CPA?

Unlike CPAs, who are skilled in managing financial records and preparing tax returns, the tax attorney is more planning and dispute-oriented; meaning they are primarily trained to help minimize a business' tax liability through the structuring of assets or to represent them through tax-related litigation.

What is the difference between a CPA and a tax preparer?

A CPA has to obtain a proper degree, pass a complicated exam, obtain professional experience, and face regulation by a state board. Without completing the proper degree, tax preparers will not have the basic accounting skills required to prepare business tax returns.

What is due diligence in tax preparation?

What is due diligence? Basically, the IRS requires that a tax preparer who prepares a return for a client that claims any of these credits or head-of-household status thoroughly interview and question the taxpayer and collect documentation to show that the taxpayer is qualified for the tax advantage.

Can a CPA represent you before the IRS?

Usually, attorneys, certified public accountants (CPAs), and enrolled agents may represent taxpayers before the IRS. Enrolled retirement plan agents, and enrolled actuaries may represent with respect to specified Internal Revenue Code sections delineated in Circular 230.

Is it worth having a CPA do your taxes?

CPAs can help you online or in person to prepare and file your necessary tax documents as well as offer advice on how to optimize your tax return. Hiring a tax professional often works to your advantage when your circumstances are complex or involve a significant amount of work.

Is it better to go to a tax preparer?

The IRS says it takes the average person about 13 hours to file Form 1040 or 1040-SR. 8 If you don't have the time to spare, then using a preparer is the better choice. Tax preparation fees vary widely, depending on the preparer's credentials, the complexity of your return, and your geographic location.

What are the four due diligence requirements for tax return preparers?

The Four Due Diligence RequirementsComplete and Submit Form 8867. (Treas. Reg. section 1.6695-2(b)(1)) ... Compute the Credits. (Treas. Reg. section 1.6695-2(b)(2)) ... Knowledge. (Treas. Reg. section 1.6695-2(b)(3)) ... Keep Records for Three Years.

How many tax due diligence requirements are there?

four due diligence requirementsmust meet four due diligence requirements. The tax benefits are the earned income tax credit (EITC), the child tax credit (CTC), the additional child tax credit (ACTC), the credit for other dependents (ODC), the American opportunity tax credit (AOTC), and head of household (HOH) filing status.

Is your tax preparer liable for mistakes?

The IRS Penalizes Tax Preparers Who Make Mistakes. If the IRS determines that your tax preparer made a mistake, this may help you in seeking to avoid fees, penalties, and interest (or having these costs paid by your tax preparer).

How much does a CPA charge for an IRS audit?

The average hourly fee for an in-person IRS audit is $150 and the average fee for an IRS audit response letter is $128.

Who can represent me with a tax audit?

Any attorney, CPA, enrolled agent, enrolled actuary or other person permitted to represent a taxpayer before the IRS, who's not disbarred or suspended from practice before the IRS, may submit a written power of attorney to represent a taxpayer before the IRS.

Can a CPA represent a taxpayer in tax court?

Tax resolution. A CPA can essentially perform all the same tax functions as a tax attorney and EA outside of representing a taxpayer in U.S. Tax Court.

What does a tax preparer do?

A tax preparer is an individual who prepares, calculates, and files income tax returns on behalf of individuals and businesses.

What is another name for a tax preparer?

Certified Public Accountant (CPA)

What's the difference between a CPA and an accountant?

A CPA is not the same as an accountant. An accountant is typically a professional who has earned a bachelor's degree in accounting. A CPA, or Certified Public Accountant, is a professional who has earned their CPA license through a combination of education, experience and examination.

What does a CPA do?

The primary task of the CPA is to audit the books of clients. If the resulting financial statements of a client meet the CPA's evaluation criteria, the CPA will issue an auditor's opinion concerning the financial statements that accompany the statements when they are issued to third parties.

What is tax due diligence?

By purchasing a company, the acquirer usually assumes liability for past tax risks. Tax due diligence is intended to present the tax situation of the company to be acquired (target), identify tax risks and ensure a tax-optimal structuring of the corporate transaction.

How is tax due diligence done – the process

In terms of process, it is advisable to work with questionnaires and data rooms when carrying out tax due diligence, in the same way as in other areas. It is highly recommended to individualise standard questionnaires in advance and to define focal points here.

How are the results of the tax due diligence processed?

The results of due diligence are regularly summarised in a tax due diligence report. Each risk is briefly described verbally and quantified as best as possible and then marked with a colour:

Tax due diligence checklist

The following checklist assists in compiling important documents for classic tax due diligence. It will also help you to identify common risk areas.

Other Systems Solution which Increase your Profits

Keep your existing healthcare provider. 500 client references. including NHL teams and national banks.

PDF Overview of our Top 5

CPA Due Diligence w ww.CPADueDiligence.com For over over 10 years, our elite community of Attorneys & CPAs has done Due Diligence on many cost-saving, tax mitigation, and wealth creation solutions. Many of our vetted solutions have NO NET COST and all have 100s of client references.

Who obtains due diligence information?

In addition to information requested from the Target, some of the due diligence information may be obtained directly by the Acquirer. Things like copies of the Target’s (and its subsidiaries) governing documents and the results of Uniform Commercial Code (UCC) and where applicable, real property lien searches, should be obtained directly by the Acquirer and its service providers.

Who reviews due diligence?

Once the due diligence information is received, the management of the Acquirer, the Acquirer’s legal counsel and accountants review the information and create a listing of additional information sought and questions raised.

What does an acquirer do with the information obtained through the due diligence process?

So what does an Acquirer do with the information obtained through the due diligence process? First, the Acquirer, after looking at the information received, needs to make a cost/benefit analysis determination of whether the transaction and the potential benefits and costs of the transaction are still attractive to the Acquirer based on what it learns about the actual inner workings of the Target and its potential for future growth.

What are the duties of the Board of Directors of the acquirer and target?

The Board of Directors of both the Acquirer and the Target will need to undertake their own due diligence to determine and confirm that any transaction is fair to the owners of the Acquirer and Target, respectively . The Boards will need to comply with all fiduciary duties relating to the transaction, including being informed regarding the terms of the transaction and potential alternatives, if the transaction will result in a sale of substantially all of the Target’s assets or securities, and need to determine that the ‘best’ price for such assets/operations is obtained.

What should the Acquirer confirm?

As part of the due diligence process the Acquirer should confirm what insurance the Target has in place, both to ensure that such insurance is adequate – if the Acquirer will be acquiring the Target and its insurance policies – and to obtain similar insurance coverage for any assets of Target which are acquired separate from the pre-existing insurance coverage.

What is due diligence for target?

All initial requests for due diligence should include requests for all correspondence received, or sent by, the Target to any government agencies and any self-regulatory agencies for the past three to five years. This would include any comment letters from the Securities and Exchange Commission (SEC) if the Target is a public company and any warnings received from any exchange on which the Target’s securities trade, as well as any notices or correspondence received from regulators regarding any non-compliance with federal or state rules and regulations.

How far back should a due diligence questionnaire go?

The due diligence questionnaire should request records going back five years or more for all issuances of securities of the Target, including common stock, preferred stock, options, warrants, convertible securities and other stock and similar rights.

What is due diligence audit?

Due diligence and audits reduce a company’s risk and exposure to bribery and provide strong evidence of compliance with anti-bribery legislation as well as protection from federal investigations.

What regulatory agencies are responsible for due diligence?

Regulatory agencies such as the DOJ and the SEC have stressed the need for companies to routinely conduct due diligence in a variety of situations and have sought to impose stringent penalties on companies that have failed to adhere to such mandates both before and after FCPA violations are discovered.

What are the consequences of not doing due diligence?

The consequences for failing to undergo proper due diligence could be severe such as civil and criminal penalties, disgorgement, prejudgment interest, imprisonment, disqualification from doing business with certain entities such as the U.S. government, and reputational harm.

Why is due diligence important?

Due diligence is important so that companies are assured that their pending transaction with the other party have an acceptable level of risk. It helps companies manage risks, assess proportionality, and detect the possibility of bribery.

What are the red flags of due diligence?

Due diligence should assess red flags such as a history of civil and/or criminal enforcement actions, negative business reputation, poor financial history, or unexplained travel expenses.

Why do we need a compliance certification?

obtain a compliance certification each year to foster an environment where bribers and corruption are not permitted

Who makes the decision of whether or not to proceed with the transaction or deal with the evaluated party?

The company makes the decision of whether or not to proceed with the transaction or deal with the evaluated party.

Popular Posts:

- 1. how to file for divorce in florida without an attorney

- 2. how to get power of attorney in nj

- 3. how to research an attorney track record

- 4. how to choose an attorney

- 5. how to fight attorney fees

- 6. which excerpt from part one of trifles most develops the motives of the county attorney?

- 7. how to find a pro bono attorney

- 8. what type of software can your parents use to create a will without visiting an attorney?

- 9. who is my district attorney

- 10. how to get power of attorney for parent with dementia