The completed Power of Attorney and Declaration of Representative Form (IRS form 2848) should be mailed to the appropriate regional IRS office. There are three national centers that receive paperwork – in Tennessee, Utah, and Pennsylvania. Consult the filing directions on the IRS Website to determine where to send your form.

Full Answer

Where to mail form 2848 IRS?

Submit Forms 2848 and 8821 Online

- Before You Get Started. If you are an e-Services user (e.g, TDS, TIN Matching) and logged in, you will need to log out of e-Services and return here to log ...

- Submit Your Form. Log in with your Secure Access unique username, password, and security code. ...

- After You Submit. ...

- Submit Forms via Fax or Mail. ...

- Frequently Asked Questions

Where to file Form 2848 with IRS?

- Receive confidential tax information

- Sign an agreement with the IRS regarding taxes, on tax returns specified on Form 2848

- Sign documents requesting additional time to assess the tax obligation, as well as extra time in order to agree to a tax adjustment

- Sign a tax return in a limited situation 3

Where and how to fax form 2848 to IRS?

- Upload your IRS form to WiseFax and select pages that you wish to fax

- Select United States as recipient’s country and enter IRS fax number

- Sign in and make a one time purchase of fax tokens, if required

- Click the “Send” button to confirm your fax

What is the tax form for power of attorney?

Tax professionals are largely ready to forge ahead to help their clients get through it, but now they may have trouble getting power of attorney forms processed. “Although the IRS informs taxpayer representatives they should anticipate long processing ...

How do I send 2848 to IRS?

Electronic Signatures Forms 2848 with an electronic signature image or digitized image of a handwritten signature may only be submitted to the IRS online at IRS.gov/Submit2848.

Where do I send a fax 2848?

Power of Attorney - Form 2848THEN use this address...Fax number*Internal Revenue Service PO Box 268, Stop 8423 Memphis, TN 38101-0268901-546-4115Internal Revenue Service 1973 N Rulon White Blvd MS 6737 Ogden, UT 84404801-620-42492 more rows•Jun 22, 2019

Can power of attorney be signed electronically IRS?

The process to mail or fax authorization forms to the IRS is still available. Signatures on mailed or faxed forms must be handwritten. Electronic signatures are not allowed.

Where do I mail paperwork to the IRS?

Alaska, Arizona, California, Colorado, Hawaii, Idaho, New Mexico, Nevada, Oregon, Utah, Washington, Wyoming: Internal Revenue Service, P.O. Box 7704, San Francisco, CA 94120-7704.

How long does it take for IRS to process form 2848?

The fax and mail options for submitting Forms 2848 and 8821 are still available, however signatures on such forms must be handwritten. Using the online option will not accelerate the time necessary for the IRS to process the authorizations, which is currently estimated to be five weeks.

Does the IRS accept electronic signatures on form 2848?

As long as you can create a Secure Access account and follow authentication procedures, you may submit a Form 2848 or 8821 with an image of an electronic signature.

How long does it take for the IRS to process a POA?

To reduce processing time, the IRS added resources from multiple sites other than the three CAF units to assist in processing. During the past year, the average time the IRS took to process a POA fluctuated from 22 days to over 70 days and is currently 29 days.

Does the IRS accept durable power of attorney?

Internal Revenue Service The IRS will accept a durable power of attorney when the document authorizes the named decision-maker to handle tax matters. But, the authorized agent will be required to execute IRS Form 2848 and file an affidavit before being recognized by the IRS.

Can you DocuSign a POA?

With DocuSign Notary, the claimant can now sign and get their POA notarized electronically and remotely — removing the hassles of meeting in person and saving time for both the signer and the company.

How do I send mail to IRS?

Mailing Tips Write both the destination and return addresses clearly or print your mailing label and postage. If your tax return is postmarked by the filing date deadline, the IRS considers it on time. Mail your return in a USPS blue collection box or at a Postal location that has a pickup time before the deadline.

What is the correct IRS address?

More In FileForm Name (To obtain a copy of a Form, Instruction, or Publication)Address to Mail Form to IRS:Form 1040-SS U.S. Self-Employment Tax Return (if enclosing a payment)Internal Revenue Service P.O. Box 1303 Charlotte, NC 28201-1303 USAForm 1040VTaxpayer or Tax Professional filing Form 1040V44 more rows•Feb 8, 2022

Is it better to fax or mail IRS?

Fax or mail, pick one. If mailing documents, use a certified mail service. Send Copies: Never ever send originals. The IRS might lose your documentation, and they certainly won't mail it back.

What does authorization of a qualifying representative do?

Your authorization of a qualifying representative will also allow that individual to receive and inspect your confidential tax information.

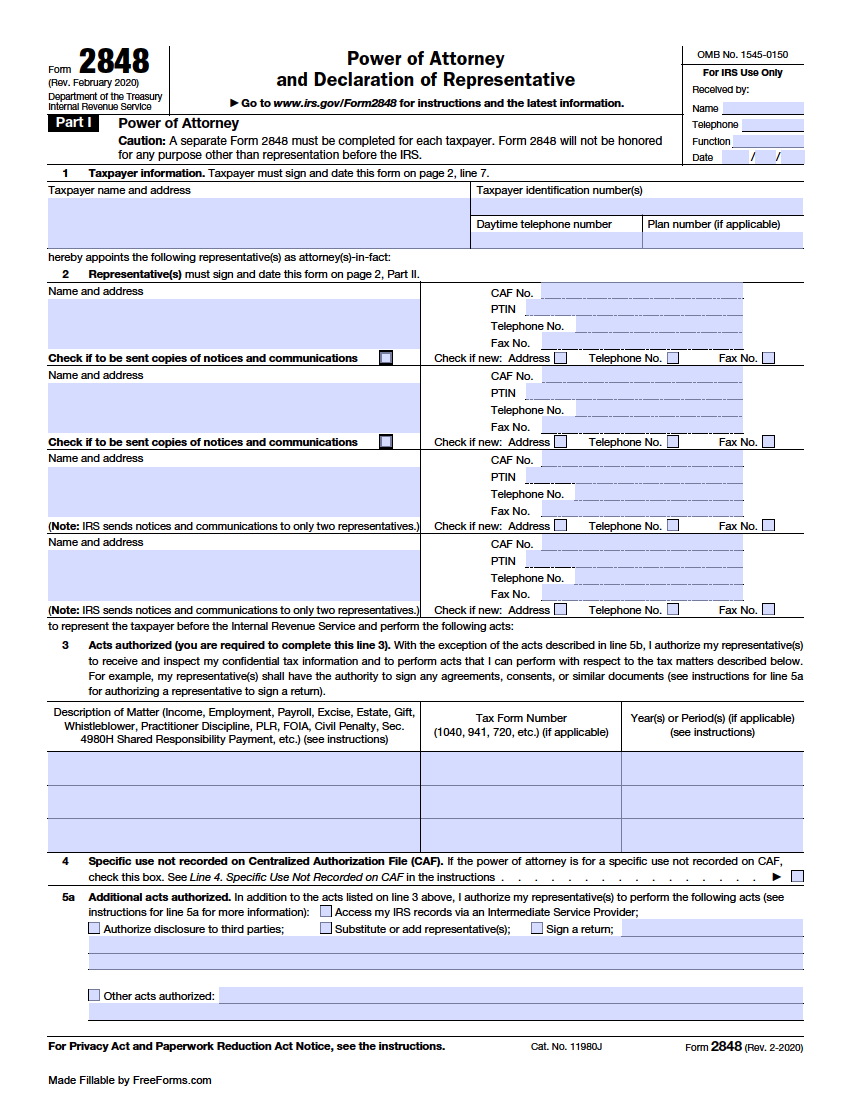

What is a 2848 form?

About Form 2848, Power of Attorney and Declaration of Representative. Use Form 2848 to authorize an individual to represent you before the IRS. The individual you authorize must be a person eligible to practice before the IRS.

How to authorize a power of attorney?

Authorize with Form 2848 - Complete and submit online, by fax or mail Form 2848, Power of Attorney and Declaration of Representative.

Where is my tax authorization?

Your Tax Information Authorization is recorded on the Centralized Authorization File (CAF) unless Line 4, Specific Use is checked. The record lets IRS assistors verify your permission to speak with your representative about your private tax-related information.

How long does a tax authorization stay in effect?

Tax Information Authorization stays in effect until you revoke the authorization or your designee withdraws it.

How to authorize a third party to file taxes?

There are different types of third party authorizations: 1 Power of Attorney - Allow someone to represent you in tax matters before the IRS. Your representative must be an individual authorized to practice before the IRS. 2 Tax Information Authorization - Appoint anyone to review and/or receive your confidential tax information for the type of tax and years/periods you determine. 3 Third Party Designee - Designate a person on your tax form to discuss that specific tax return and year with the IRS. 4 Oral Disclosure - Authorize the IRS to disclose your tax information to a person you bring into a phone conversation or meeting with us about a specific tax issue.

What is a tax information authorization?

A Tax Information Authorization lets you: Appoint a designee to review and/or receive your confidential information verbally or in writing for the tax matters and years/periods you specify. Disclose your tax information for a purpose other than resolving a tax matter.

How long does a power of attorney stay in effect?

Power of Attorney stays in effect until you revoke the authorization or your representative withdraws it. When you revoke Power of Attorney, your representative will no longer receive your confidential tax information or represent you before the IRS for the matters and periods listed in the authorization.

Why do we disclose tax returns?

The tax return information we may disclose to allow the third party to assist you.

How to represent yourself before the IRS?

If you choose to have someone represent you, your representative must be an individual authorized to practice before the IRS. Submit a power of attorney if you want to authorize an individual to represent you before the IRS. You can use Form 2848, Power of Attorney and Declaration of Representative for this purpose. Your signature on the Form 2848 allows the individual or individuals named to represent you before the IRS and to receive your tax information for the matter (s) and tax year (s)/period (s) specified on the Form 2848.

What is a 2848 form?

You can use Form 2848, Power of Attorney and Declaration of Representative for this purpose. Your signature on the Form 2848 allows the individual or individuals named to represent you before the IRS and to receive your tax information for the matter (s) and tax year (s)/period (s) specified on the Form 2848.

What is a power of attorney for IRS?

Except as specified below or in other IRS guidance, this power of attorney authorizes the listed representative (s) to inspect and/or receive confidential tax information and to perform all acts (that is, sign agreements, consents, waivers, or other documents) that you can perform with respect to matters described in the power of attorney. Representatives are not authorized to endorse or otherwise negotiate any check (including directing or accepting payment by any means, electronic or otherwise, into an account owned or controlled by the representative or any firm or other entity with whom the representative is associated) issued by the government in respect of a federal tax liability. Additionally, unless specifically provided in the power of attorney, this authorization does not include the power to substitute or add another representative, the power to sign certain returns, the power to execute a request for disclosure of tax returns or return information to a third party, or to access IRS records via an Intermediate Service Provider. Representatives are not authorized to sign Form 907, Agreement to Extend the Time to Bring Suit, unless language to cover the signing is added on line 5a. See Line 5a. Additional Acts Authorized, later, for more information regarding specific authorities.

Where to enter BBA in a power of attorney?

For powers of attorney related to the centralized partnership audit regime, enter “Centralized Partnership Audit Regime (BBA)” in the "Description of Matter" column on line 3, then enter the form number (for example, 1065) and tax year in the appropriate column (s).

What is Form 2848?

The individual you authorize must be eligible to practice before the IRS. Form 2848, Part II, Declaration of Representative, lists eligible designations in items (a)– (r). Your authorization of an eligible representative will also allow that individual to inspect and/or receive your confidential tax information.

What is the APO number for Guam?

855-214-7522. All APO and FPO addresses, American Samoa, the Commonwealth of the Northern Mariana Islands, Guam, the U.S. Virgin Islands, Puerto Rico, a foreign country, or otherwise outside the United States. Internal Revenue Service. International CAF Team.

Can a law student represent a taxpayer?

You must receive permission to represent taxpayers before the IRS by virtue of your status as a law, business, or accounting student working in an LITC or STCP under section 10.7 (d) of Circular 230. Law graduates in an LITC or STCP may also represent taxpayers under the "Qualifying Student" designation in Part II of Form 2848. Be sure to attach a copy of the letter from the Taxpayer Advocate Service authorizing practice before the IRS.

Can I represent a business before the IRS?

You must receive permission to represent taxpayers before the IRS by virtue of your status as a law, business , or accounting student working in an LITC or STCP under section 10.7 (d) of Circular 230. Law graduates in an LITC or STCP may also represent taxpayers under the "k" designation in Part II of Form 2848. Be sure to attach a copy of the letter from the Taxpayer Advocate Service authorizing practice before the IRS.

Can an unenrolled return preparer represent taxpayers?

Unenrolled return preparers cannot represent taxpayers, regardless of the circumstances requiring representation, before appeals officers, revenue officers, attorneys from the Office of Chief Counsel, or similar officers or employees of the Internal Revenue Service or the Department of the Treasury.

What is an addition to a POA?

Additions/Deletions to Authorized Acts Under POA - Describe any specific additions or deletions to the acts otherwise authorized by this Power of Attorney.

How to access Form 2848?

To access Form 2848, from the Main Menu of the Tax Return (Form 1040) select: Plan Number - The program will pull the taxpayer name (s), address, SSN (s) and daytime phone number. If an Employer Identification Number and/or Plan Number applies, enter these items in this menu. Select New to enter in the information for the representative.

What is a 2848 form?

Form 2848 is used to designate an individual to represent the taxpayer before the IRS and to allow the representative to perform all tax acts that the taxpayer would normally take care of. A taxpayer can limit which duties their representative can perform by attaching a statement to the power of attorney explaining exactly what their duties will be. Without limitations, the representative will be able to sign consents extending the time to assess tax, record the interview, sign waivers agreeing to tax adjustments, sign closing agreements, and also receive refund checks.

What to do if CAF number has not been assigned?

Check the appropriate box to indicate if either the address, telephone number or fax number is new since a CAF number has been assigned. Select the designation for the representative.

Can a power of attorney be recorded on a CAF?

Is the Power of Attorney recorded on a CAF file - If the Power of Attorney is for a use that will not be listed on the CAF, change the answer to YES. The authorized representative should mail or fax the Power of Attorney to the IRS office handling this matter.

Popular Posts:

- 1. how to file for divorce in florida without an attorney

- 2. how to get power of attorney in nj

- 3. how to research an attorney track record

- 4. how to choose an attorney

- 5. how to fight attorney fees

- 6. which excerpt from part one of trifles most develops the motives of the county attorney?

- 7. how to find a pro bono attorney

- 8. what type of software can your parents use to create a will without visiting an attorney?

- 9. who is my district attorney

- 10. how to get power of attorney for parent with dementia