An agent with a valid power of attorney for finances may be able to:

- Access the principal’s financial accounts to pay for health care, housing needs and other bills.

- File taxes on behalf of the principal.

- Make investment decisions on behalf of the principal.

- Collect the principal’s debts.

- Manage the principal’s property.

- Apply for public benefits for the principal, such as Medicaid, veterans benefits, etc.

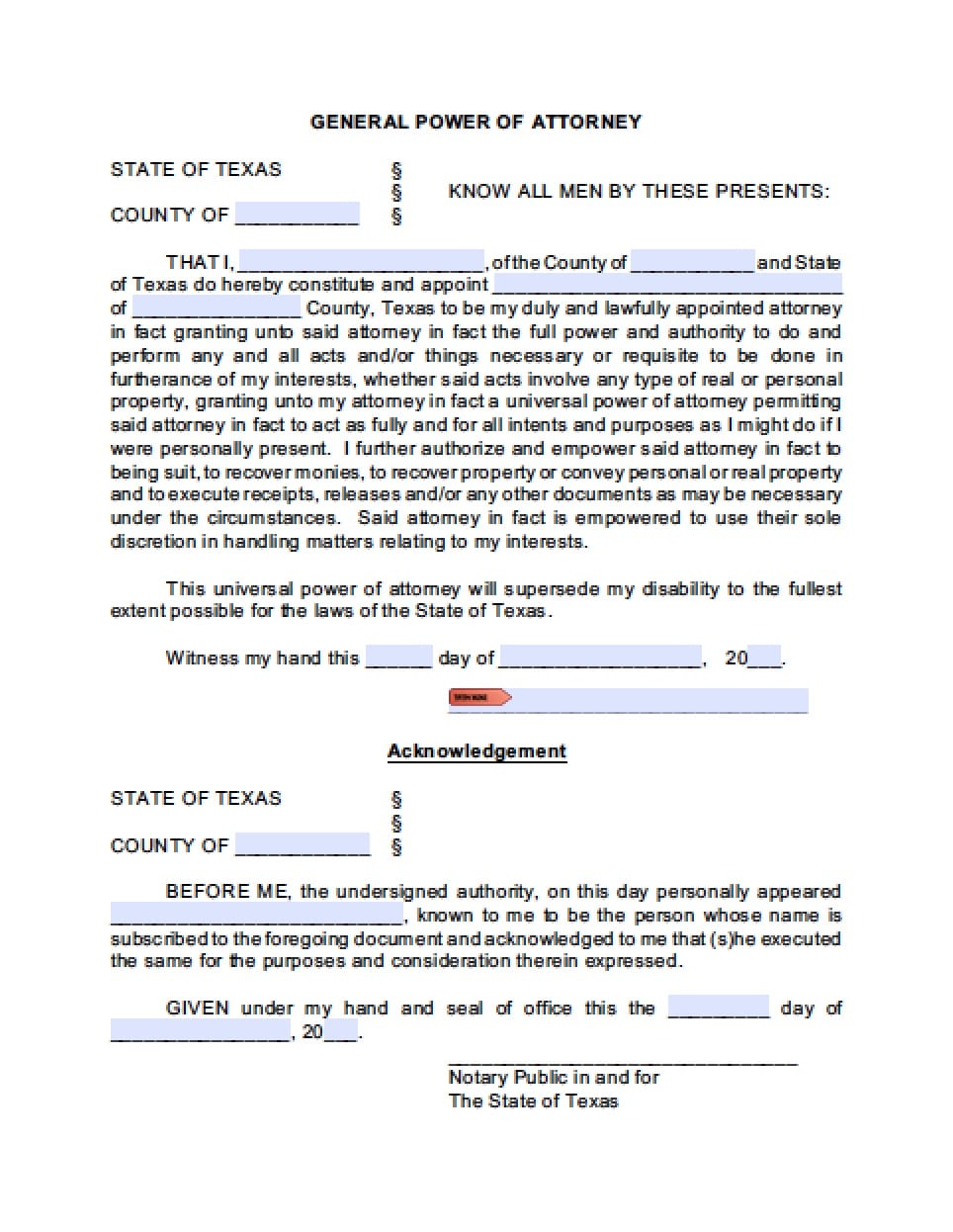

A financial power of attorney (POA) is a legal document that grants a trusted agent the authority to act on behalf of the principal-agent in financial matters. The former is also referred to as the attorney-in-fact while the principal-agent is the person who grants the authority.

Full

AnswerWhat is a financial power of attorney?

Aug 16, 2020 · A financial power of attorney is a legal document that grants a trusted agent the authority to act on behalf of the principal in financial matters. Education General

What can an agent do under a power of attorney?

May 04, 2022 · Power of attorney doesn’t mean you’ve relinquished control of your assets; having an agent just means that your agent can also act for you, if need be.

Who needs a power of attorney form?

May 02, 2022 · A financial power of attorney is a particular type of POA that authorizes someone to act on your behalf in financial matters. Many states have …

What is a special power of attorney (POA)?

Sep 27, 2021 · A financial power of attorney is just a document you need when you want to grant someone else the power to make money decisions for you. And it’s usually created alongside your will. This kind of POA is written specifically to let someone else act as your legal rep for financial matters.

What are the three basic types of powers of attorney?

The three most common types of powers of attorney that delegate authority to an agent to handle your financial affairs are the following: General power of attorney. Limited power of attorney. Durable power of attorney.

What is the best power of attorney to have?

You can write a POA in two forms: general or limited. A general power of attorney allows the agent to make a wide range of decisions. This is your best option if you want to maximize the person's freedom to handle your assets and manage your care.Mar 19, 2019

What three decisions Cannot be made by a legal power of attorney?

You cannot give an attorney the power to: act in a way or make a decision that you cannot normally do yourself – for example, anything outside the law. consent to a deprivation of liberty being imposed on you, without a court order.

What is the difference between power of attorney and lasting power of attorney?

An ordinary power of attorney is only valid while you have the mental capacity to make your own decisions. If you want someone to be able to act on your behalf if there comes a time when you don't have the mental capacity to make your own decisions you should consider setting up a lasting power of attorney.

What is financial power of attorney?

What Is a Financial Power of Attorney? A financial power of attorney is a particular type of POA that authorizes someone to act on your behalf in financial matters. Many states have an official financial power of attorney form.

Do banks have power of attorney?

Many states have an official durable power of attorney form, which is usually a durable financial power of attorney form. Some banks and brokerage firms have their own power of attorney forms. Also, for buying or selling real property, a title insurance company, lender or closing agent may require the use of their form.

Can a third party accept a power of attorney?

Generally, a third party is not required to accept a power of attorney. However, some state laws provide for penalties for a third party who refuses to accept a power of attorney using the state’s official form.

How does a POA work?

Financial Power of Attorney: How It Works. A durable financial power of attorney can avoid financial disaster in the event you become incapacitated. You can also use a POA to allow someone to transact business for you if you are out of town or otherwise unavailable. If you need to give another person the ability to conduct your financial matters ...

What is a POA?

What Is Power of Attorney? A power of attorney (or POA) is a legal document that authorizes someone to act on your behalf. The person who gives the authority is called the "principal," and the person who has the authority to act for the principal is called the "agent," or the "attorney-in-fact.".

When does a POA become effective?

When Does a Power of Attorney Become Effective? Depending upon how it is worded, a POA can either become effective immediately, or upon the occurrence of a future event. If the POA is effective immediately, your agent may act on your behalf even if you are available and not incapacitated. This is done when someone can’t be present ...

What is incapacity in medical terms?

Incapacity is where the principal is certified by one or more physicians to be either mentally or physically unable to make decisions. This could be due to such things as mental illness, Alzheimer’s disease, being in a coma, or being otherwise unable to communicate.

How to make a POA?

A number of things can make a financial POA kaput: 1 The death of the principal 2 The principal choosing to revoke the power at any time 3 A court ruling it invalid 4 The principal’s agent becoming unable to fulfill their duties as financial POA (this can be avoided by naming a successor agent in the document) 5 In some states, when the principal has both 1) named their spouse as the agent, and 2) later divorced their spouse 6 And generally speaking, if the principal becomes incapacitated unless the POA is worded to say that the agent’s authority should continue anyway

What is a financial power of attorney?

A financial power of attorney is just a document you need when you want to grant someone else the power to make money decisions for you. And it’s usually created alongside your will. This kind of POA is written specifically to let someone else act as your legal rep for financial matters. Much like other powers of attorney, ...

What is a financial POA?

Just as a medical POA only applies to medical choices someone makes for you, the financial POA extends no further than the right for someone else to make money decisions if and when you’re unavailable to do so yourself. (In case you’re wondering, you need both kinds of POA to have full protection.)

What is a POA in financial planning?

With a financial POA, your agent can keep everything moving smoothly with your money. Like most legal docs, the main purpose for creating a financial POA is to protect you and your family from a preventable legal battle.

Is Joe a good agent?

Yeah, Joe could be an awesome agent. For many people, the obvious choice is their spouse. If either of you travel a lot for work, appointing the other as an agent in your financial POA makes a lot of sense. Or maybe you know someone outside your family who just has good character and financial smarts.

What is a Financial Power of Attorney?

A Financial Power of Attorney is the part of your Estate Plan that allows you to grant authority to someone you trust to handle your financial matters. Your Financial POA (also known as an Attorney-in-Fact) can step in when and if you’re ever unable to make financial decisions on your own due to incapacitation, death or absence.

What is a Durable Financial Power of Attorney?

A Durable Financial Power of Attorney is just the term used that denotes someone can act even after you become incapacitated and can’t express your will or make decisions. It’s not uncommon to wonder what powers does a Durable Power of Attorney have - and we’ll cover that in a bit.

How to Choose a Financial Power of Attorney

Choosing your Financial POA can be a bit daunting, but you want to take the time to make sure you’re confident with your decision and that you trust the person you name. In the long run, it will be well worth the time you’ll spend deciding.

Why do I Need a Financial Power of Attorney?

A Financial Power of Attorney is a component of your Estate Plan that ensures financial matters in your estate and are handled appropriately and responsibly. Knowing that your financial responsibilities, investments, retirement, bills and everything else in your financial world is in good hands can be a great source of comfort.

What powers can a power of attorney have?

A power of attorney may be a good idea for people who are unable or who may become unable in the future to manage their financial affairs or make other decisions for themselves. Examples of powers people can give to their agent are: 1 To use a person’s assets to pay their everyday living expenses. 2 To manage benefits from Social Security, Medicare, or other government programs. 3 To handle transactions with their bank and other financial institutions. 4 To file and pay a person’s taxes. 5 To manage a person’s retirement accounts.

Do banks have power of attorney?

In addition, some banks and financial companies have their own power of attorney forms. Preparing additional, organization-specific forms may make it easier for an agent to work with certain organizations with which the principal does business. For general information (not legal advice) and sample forms, contact:

What is the difference between a general power of attorney and a limited power of attorney?

A general power of attorney gives an agent the ability to act on a person’s behalf in all of their affairs, while a limited power of attorney grants an agent this authority only in specific situations.

Can a principal revoke a power of attorney?

A principal can also revoke a power of attorney. For example, somebody facing surgery may complete a power of attorney on a temporary basis, but then revoke it once they are healed and out of the hospital.

What is the job of a Social Security administrator?

To manage benefits from Social Security, Medicare, or other government programs. To handle transactions with their bank and other financial institutions. To file and pay a person’s taxes. To manage a person’s retirement accounts.

What is the purpose of a retirement account?

To use a person’s assets to pay their everyday living expenses. To manage benefits from Social Security, Medicare, or other government programs. To handle transactions with their bank and other financial institutions. To file and pay a person’s taxes. To manage a person’s retirement accounts.

What is a power of attorney for health care?

A health care power of attorney grants your agent authority to make medical decisions for you if you are unconscious, mentally incompetent, or otherwise unable to make decisions on your own. While not the same thing as a living will, many states allow you to include your preference about being kept on life support.

Is a power of attorney valid if you are mentally competent?

A power of attorney is valid only if you are mentally competent when you sign it and, in some cases, incompetent when it goes into effect. If you think your mental capability may be questioned, have a doctor verify it in writing.

What is a power of attorney?

A power of attorney is a document that lets you name someone to make decisions on your behalf. This appointment can take effect immediately if you become unable to make those decisions on your own.

What is a POA?

A power of attorney (POA) is a document that allows you to appoint a person or organization to manage your property, financial, or medical affairs if you become unable to do so.

What powers can an agent exercise?

You can specify exactly what powers an agent may exercise by signing a special power of attorney. This is often used when one cannot handle certain affairs due to other commitments or health reasons. Selling property (personal and real), managing real estate, collecting debts, and handling business transactions are some ...

Why is it important to have an agent?

It is important for an agent to keep accurate records of all transactions done on your behalf and to provide you with periodic updates to keep you informed. If you are unable to review updates yourself, direct your agent to give an account to a third party.

Why do you need multiple agents?

Multiple agents can ensure more sound decisions, acting as checks and balances against one another. The downside is that multiple agents can disagree and one person's schedule can potentially delay important transactions or signings of legal documents. If you appoint only one agent, have a backup.

What is the CFPB?

The Consumer Financial Protection Bureau, or the CFPB, is focused on making markets for consumer financial products and services work for families — whether they are applying for a mortgage, choosing among credit cards, or using any number of other consumer financial products. We empower consumers to take more control over their financial lives.

Who has authority to make decisions for Martina?

Other fiduciaries may have authority to make decisions for Martina. For example, she may have a guardian of property, a representative payee who handles Social Security benefits, or a VA fiduciary who handles veterans benefits. It is important to work with these other fiduciaries , and keep them informed.

What is Martina's duty?

Because you are dealing with Martina’s money and property, your duty is to make decisions that are best for her. This means you must ignore your own interests and needs, or the interests and needs of other people.

What did you use Martina's money for?

You used Martina’s money to buy a car. You use it to drive her to appointments, but most of the time you drive the car just for your own needs. This may be a conflict of interest.

Popular Posts:

- 1. how to file for divorce in florida without an attorney

- 2. how to get power of attorney in nj

- 3. how to research an attorney track record

- 4. how to choose an attorney

- 5. how to fight attorney fees

- 6. which excerpt from part one of trifles most develops the motives of the county attorney?

- 7. how to find a pro bono attorney

- 8. what type of software can your parents use to create a will without visiting an attorney?

- 9. who is my district attorney

- 10. how to get power of attorney for parent with dementia