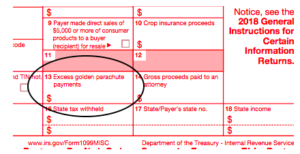

Form 1099-MISC Miscellaneous Income, Box 10 shows gross proceeds paid to an attorney in connection with legal services. These amounts are generally reported on Schedule C (Form 1040) Profit or Loss From Business. Enter only the taxable portion as income on your return.

Do I issue a 1099 to my attorney?

Form 1099-MISC - Gross Proceeds Paid to an Attorney. Form 1099-MISC, Box 14 shows gross proceeds paid to an attorney in connection with legal services. These amounts are generally reported on Schedule C. Enter only the taxable portion as income on your return. To enter or review the information for Form 1099-MISC, Box 14 Gross proceeds paid to an attorney:

Do payments to law firms require 1099?

From within your Form 1099-MISC, continue with the interview process until you reach the screen titled 1099-MISC: Enter information on form. Click the data entry field below Box 10 - Gross proceeds paid to an attorney, and type your amount. Was this helpful to you?

Should Attorneys receive a 1099?

· Here are the steps to enter your 1099-MISC with Box 14: Sign into your account and click " Take me to my return " In the Search box (upper right of program) search ' 1099 misc …

What dollar amount requires a 1099?

Form 1099-MISC Miscellaneous Income, Box 10 shows gross proceeds paid to an attorney in connection with legal services. These amounts are generally reported on Schedule C (Form …

What are gross proceeds paid to an attorney on 1099-MISC?

Gross proceeds are payments that: Are made to an attorney in the course of your trade or business in connection with legal services, but not for the attorney's services, for example, as in a settlement agreement; Total $600 or more; and. Are not reportable by you in box 7.

Do attorneys fees go on 1099-MISC or 1099-NEC?

When to report attorney payments on a 1099-NEC Rule of thumb: Report payments to an attorney on Form 1099-NEC if you were their client. Of course, the reporting requirements we went through above still apply: The payments need to be $600 or more and rendered for work-related services.

Do I send a 1099 to a law firm?

Issue a Form 1099-MISC to the litigant's attorney when fees are awarded. Anyone making a payment to an attorney “in connection with legal services” or in the course of a trade or business must issue a Form 1099 regardless of whether who actually retained the firm.

What does gross proceeds mean on a 1099?

Gross proceeds means any cash received or to be. received for the real property by or on behalf of the transferor, including the stated principal amount of a note payable to or for. the benefit of the transferor and including a note or mortgage. paid off at settlement.

Do I have to send a 1099 for attorney fees?

Lawyers need to send Forms 1099, too You should make a practice of issuing 1099s when required. For example, suppose you are lead counsel in a case and receive a $1 million fee, but only keep $400,000, paying the other $600,000 to other lawyers or law firms. You must issue Forms 1099s to all of your co-counsel.

Where do legal fees go on 1099?

Attorney fees paid in the course of your trade or business for services an attorney renders to you are reported in box 1 of Form 1099-NEC. Gross proceeds paid to an attorney in connection with legal services, but not for the attorney's services, are reported in box 10 of Form 1099-MISC.

Are gross proceeds lawyers taxable?

The IRS does not track amounts reported as gross proceeds paid to an attorney on Form 1099 in the way it treats say “other income” on from 1099-MISC Box 3. Therefore, the lawyer should simply report whatever portion of the reported payment (if any) is income to the lawyer.

What is listed in Box 4 on a 1099-MISC?

Box 1: Rents paid for $600 or more. Box 2: Royalties paid for $10 or more. Box 3: Other types of payments that are not considered wages, like prizes or awards. Box 4: Federal income tax withheld.

Do I send my accountant a 1099?

If the accountant is part of a corporation, you do not need to file a 1099. However, if the accountant is not part of a corporation, you might need to file a 1099. This includes accountants that are classified as a partnership or are independent contractors.

Where do I report gross proceeds from 1099 s?

If the 1099-S was for the sale of business or rental property, then it's reportable on IRS Form 4797 and Schedule D: From within your TaxAct return (Online or Desktop) click Federal. On smaller devices, click in the upper left-hand corner, then select Federal.

Are gross proceeds considered income?

Gross income includes all income you receive that isn't explicitly exempt from taxation under the Internal Revenue Code (IRC). Taxable income is the portion of your gross income that's actually subject to taxation. Deductions are subtracted from gross income to arrive at your amount of taxable income.

What is the difference between net proceeds and gross proceeds?

The proceeds received before any deductions are made are known as gross proceeds, and they comprise all the expenses incurred in the transaction such as legal fees, shipping costs, and broker commissions. Net proceeds equal the gross proceeds minus all the costs.

How to report a 1099 to an attorney?

To report payments to an attorney on Form 1099-MISC, you must obtain the attorney's TIN. You may use Form W-9, Request for Taxpayer Identification Number and Certification, to obtain the attorney's TIN. An attorney is required to promptly supply its TIN whether it is a corporation or other entity, but the attorney is not required to certify its TIN. If the attorney fails to provide its TIN, the attorney may be subject to a penalty under section 6723 and its regulations, and you must backup withhold on the reportable payments.

What is attorney fee on 1099?

The term "attorney" includes a law firm or other provider of legal services. Attorneys' fees of $600 or more paid in the course of your trade or business are reportable in box 1 of Form 1099-NEC, under section 6041A(a)(1). Gross proceeds paid to attorneys. Under section 6045(f), report in box 10 payments that:

What boxes are required to report backup withholding?

For example, persons who have not furnished their TINs to you are subject to withholding on payments required to be reported in boxes 1, 2 (net of severance taxes), 3, 5 (to the extent paid in cash), 6, 8, 9, and 10. For more information on backup withholding, including the rate, see part N in the 2020 General Instructions for Certain Information Returns.

Do you have to report 1099-MISC?

However, you do not have to report these payments on Form 1099-MISC if you paid them to a real estate agent or property manager. But the real estate agent or property manager must use Form 1099-MISC to report the rent paid over to the property owner. See Regulations sections 1.6041-3(d) and 1.6041-1(e)(5), Example 5.

How much do you report royalty payments on a 1099?

Enter gross royalty payments (or similar amounts) of $10 or more. Report royalties from oil, gas, or other mineral properties before reduction for severance and other taxes that may have been withheld and paid. Do not include surface royalties. They should be reported in box 1. Do not report oil or gas payments for a working interest in box 2; report payments for working interests in box 1 of Form 1099-NEC. Do not report timber royalties made under a pay-as-cut contract; report these timber royalties on Form 1099-S, Proceeds From Real Estate Transactions.

Do you report death benefits on 1099-MISC?

Death benefits from nonqualified deferred compensation plans or section 457 plans paid to the estate or beneficiary of a deceased employee are reportable on Form 1099-MISC. Do not report these death benefits on Form 1099-R. However, if the benefits are from a qualified plan, report them on Form 1099-R.

Do you report attorney fees on 1099?

Are not reportable by you in box 1 of Form 1099-NEC. Generally, you are not required to report the claimant's attorney's fees. For example, an insurance company pays a claimant's attorney $100,000 to settle a claim. The insurance company reports the payment as gross proceeds of $100,000 in box 10.

What is attorney fee on 1099?

The term "attorney" includes a law firm or other provider of legal services. Attorneys' fees of $600 or more paid in the course of your trade or business are reportable in box 1 of Form 1099-NEC, under section 6041A (a) (1).

Who is required to file 1099-MISC?

File Form 1099-MISC, Miscellaneous Information, for each person in the course of your business to whom you have paid the following during the year.

How much cash do you have to pay for a fish resale?

If you are in the trade or business of purchasing fish for resale, you must report total cash payments of $600 or more paid during the year to any person who is engaged in the trade or business of catching fish. You are required to keep records showing the date and amount of each cash payment made during the year, but you must report only the total amount paid for the year on Form 1099-MISC.

How much do you report royalty payments on a 1099?

Enter gross royalty payments (or similar amounts) of $10 or more. Report royalties from oil, gas, or other mineral properties before reduction for severance and other taxes that may have been withheld and paid. Do not include surface royalties. They should be reported in box 1. Do not report oil or gas payments for a working interest in box 2; report payments for working interests in box 1 of Form 1099-NEC. Do not report timber royalties made under a pay-as-cut contract; report these timber royalties on Form 1099-S, Proceeds From Real Estate Transactions.

Is canceled debt a 1099?

A canceled debt is not reportable on Form 1099-MISC. Canceled debts reportable under section 6050P must be reported on Form 1099-C. See the Instructions for Forms 1099-A and 1099-C.

What to report on W-2 after death?

When an employee dies during the year, you must report the accrued wages, vacation pay, and other compensation paid after the date of death. If you made the payment in the same year the employee died, you must withhold social security and Medicare taxes on the payment and report them only as social security and Medicare wages on the employee's Form W-2 to ensure that proper social security and Medicare credit is received. On the Form W-2, show the payment as social security wages (box 3) and Medicare wages and tips (box 5) and the social security and Medicare taxes withheld in boxes 4 and 6; do not show the payment in box 1 of Form W-2.

Do you report death benefits on 1099-MISC?

Death benefits from nonqualified deferred compensation plans or section 457 plans paid to the estate or beneficiary of a deceased employee are reportable on Form 1099-MISC. Do not report these death benefits on Form 1099-R. However, if the benefits are from a qualified plan, report them on Form 1099-R.

Where are attorney payments reported on a 1099?

Certain attorney and law firm payments are reported in Box 10 of the Form 1099-MISC, not the Form 1099-NEC, if:

What is an attorney 1099?

Under IRS guidance, the term “ attorney " includes a law firm or any other legal services provider on behalf of your business or trade. Remember, that 1099-NECs is for services that contribute to your business, not your personal affairs.

What is a 1099 exception?

One exception to the rules for Forms 1099 applies to payments for physical sickness or personal physical injuries settlement checks.

Where to report settlement check on 1099?

You report the $100,000 (settlement check) in Box 10 of the 1099-MISC as gross proceeds paid to an attorney; and

What box is non-employee compensation on 1099?

By reporting non-employee compensation in Box 1 of the 1099-NEC, the IRS is tipped off that the recipient of those fees reported may be a self-employed individual, thus subject to self-employment tax in addition to federal and/or state income tax. Self-employed individuals pay 100% of self-employment tax, where W-2 employees pay half, ...

What is a 1099 NEC?

You should use the Form 1099-NEC to report non-employee compensation, such as independent contractor compensation. Non-employee compensation includes fees, commissions, benefits, prizes and awards, and other forms of payment, as identified by the IRS. Any payment payable to a 1099 lawyer is reported even if all the client’s money is used ...

What is the most common 1099?

Multiple types of Form 1099s exist; however, two of the most common are Form 1099-MISC information returns and, starting for the 2020 tax year, Form 1099-NEC. Small businesses, independent contractors, and other self-employed individuals must understand the new Form 1099-NEC filing rules to satisfy their tax reporting responsibility.

Where do federal withholdings flow?

However, federal and state tax withheld entered on this screen do flow to the appropriate line of the tax return (Form 1040, line 25b, for federal amounts). This withholding should not be duplicated or re-entered anywhere else in the tax return.

What form is Schedule 1 on?

This amount will flow to Form 1040, Schedule 1, as Other Income.

Can ProConnect calculate additional taxes?

ProConnect Tax can only calculate the additional tax if the NQDC income was entered on the Wages screen (box 12, Code Z). For 1099-MISC income, you must manually calculate the tax amount.

What are gross proceeds on a 1099?

What are gross proceeds and are they reportable on a 1099-MISC form? Gross proceeds are payments that: Are made to an attorney in the course of your trade or business in connection with legal services, but not for the attorney’s services, for example, as in a settlement agreement; Are not reportable by you in box 7.

What box is the $100,000 payment in?

The insurance company reports the payment as gross proceeds of $100,000 in box 14. However, the insurance company does not have a reporting requirement for the claimant’s attorney’s fees subsequently paid from these funds. These rules apply whether or not:

Do you report attorney fees in box 7?

Are not reportable by you in box 7. Generally, you are not required to report the claimant’s attorney’s fees. For example, an insurance company pays a claimant’s attorney $100,000 to settle a claim. The insurance company reports the payment as gross proceeds of $100,000 in box 14. However, the insurance company does not have a reporting requirement ...

Is an attorney the exclusive payee?

These rules apply whether or not: The legal services are provided to the payer, The attorney is the exclusive payee (for example, the attorney’s and claimant’s names are on one check) or, Other information returns are required for some or all of a payment under another section of the Code, such as section 6041.

Popular Posts:

- 1. how to file for divorce in florida without an attorney

- 2. how to get power of attorney in nj

- 3. how to research an attorney track record

- 4. how to choose an attorney

- 5. how to fight attorney fees

- 6. which excerpt from part one of trifles most develops the motives of the county attorney?

- 7. how to find a pro bono attorney

- 8. what type of software can your parents use to create a will without visiting an attorney?

- 9. who is my district attorney

- 10. how to get power of attorney for parent with dementia