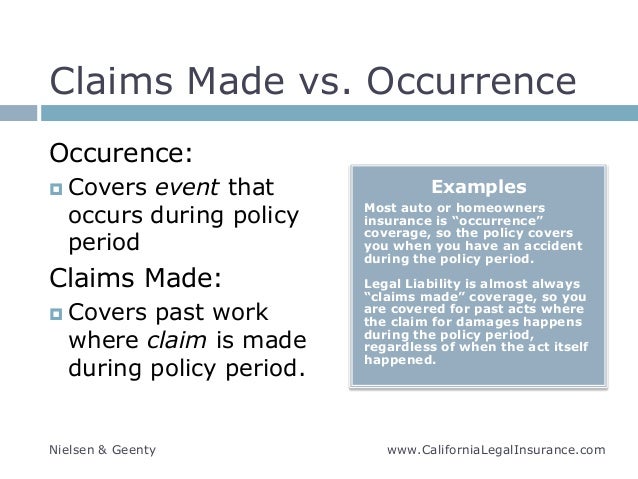

A claims-made policy covers the insured for an incident that occurred during the policy period and was reported as a claim while the policy remained in force. When you start a claims-made policy, the original inception date, known as the retroactive date, becomes a permanent part of the claims-made policy.

Full

AnswerWhat is claims made?

A claims-made policy covers the insured for an incident that occurred during the policy period and was reported as a claim while the policy remained in force. When you start a claims-made policy, the original inception date, known as the retroactive date, becomes a permanent part of the claims-made policy.

What is occurrence based malpractice insurance?

The minimum malpractice insurance limit is $100,000 per claim/$300,000 annual agg-regate. This means that the insurer will pay a maximum of $100,000 for defense and indemnity costs for any one claim made against your firm, and a maximum of $300,000 for all claims made against your firm during the policy year.

What is malpractice insurance?

Mar 30, 2015 · Legal Malpractice Insurance: Claims-Made Coverage, Part 1 of 5: How It Differs From Occurrence Coverage. For decades, all property-casualty insurance polices were occurrence policies, which cover claims that arise out of incidents that happen during the policy period, regardless of when the claims are made.

What is malpractice tail coverage?

A claims-made policy will only provide coverage if the policy is in effect both when the incident took place and when a lawsuit is filed. As can be seen, this requires that coverage must extend for a significant period of time to provide adequate protection since a considerable amount of time may elapse between when an incident may have occurred and when a claim is made.

What is the difference between claims made and occurrence?

An occurrence policy has lifetime coverage for the incidents that occur during a policy period, regardless of when the claim is reported. A claims-made policy only covers incidents that happen and are reported within the policy's time frame, unless a 'tail' is purchased.Nov 5, 2018

What is the determining factor in claims made malpractice insurance?

In order for an incident to be covered under a claims-made policy, two things must be true. First, you need to have insurance when the claim is made. Second, your prior acts date contained in your policy must be on or before the date the incident occurred.Oct 21, 2021

What's better claims made or occurrence?

Claims-made coverage is portable. You can take the coverage from one insurance company to another. The advantage to an occurrence policy is its permanence. The period of time you are insured under an occurrence policy is protected forever by the policy you had that year.

What is a claims made basis?

Claims-Made Basis — a form of reinsurance under which the date of the claim report is deemed to be the date of the loss event. ... A claims-made agreement is said to "cut off the tail" on liability business by not covering claims reported after the term of the reinsurance agreement—unless extended by special agreement.

What is a claims made endorsement?

Claims-Made Policy — a policy providing coverage that is triggered when a claim is made against the insured during the policy period, regardless of when the wrongful act that gave rise to the claim took place.

What is the difference between claims made and occurrence malpractice insurance?

An occurrence policy provides coverage for alleged incidents (injuries) that happened during the policy year regardless of when the claim is reported to the carrier. ... The renewed claims made policy covers claims that come in during the policy year for incidents that occurred on or after the retroactive date.

What does a claims-made policy mean?

Insurance companies commonly write policies on a claims-made form. This means your insurer helps cover claims filed during your policy period. There are two features of a claims-made policy that can affect coverage: Retroactive date: Your policy provides coverage if an incident occurs on or after a specified date.

How does claims made coverage work?

A claims-made policy refers to an insurance policy that provides coverage when a claim is made against it, regardless of when the claim event occurred. A claims-made policy is a popular option for when there is a delay between when events occur and when claimants file claims.

What types of policies are claims made?

Insurers typically use claims-made policy forms for professional liability insurance (also called errors and omission insurance or E&O) and directors and officers insurance (D&O).

Why is professional indemnity on a claims made basis?

Professional indemnity cover is usually offered on a claims-made basis. This means that your insurer will only cover you for claims that are brought against you during the term of your policy. ... This covers you for any new claims that are brought against you after your professional indemnity insurance has expired.

Who publishes legal malpractice FAQs?

Legal Malpractice FAQs is published by Lawyers Insurance Group, legal malpractice insurance brokers. Our mission is to obtain the best terms available in the market for your firm. We accomplish this by scouring the market on firms’ behalf, leveraging our access to dozens of “A”-rated legal malpractice insurers.

How much does malpractice insurance cost?

This means that the insurer will pay a maximum of $100,000 for defense and indemnity costs for any one claim made against your firm, and a maximum of $300,000 for all claims made against your firm during the policy year.

What are legal services?

Here’s a representative definition of “legal services”, from CNA’s policy: 1 A.”services, performed by an Insured for others as a lawyer, arbitrator, mediator, title agent or other neutral fact finder or as a notary public. 2 B. services performed by an Insured as an administrator, conservator, receiver, executor, guardian, trustee or in any other fiduciary capacity and any investment advice given in connection with such services;”

What is defense indemnity?

Defense costs and indemnity payments incurred to resolve claims filed against an attorney for acts/errors/omissions made in the course of providing legal services on behalf of the named insured, i.e., the entity (firm or individual) that bought the policy.

What is insurance broker?

Insurance brokers – brokers (which is what we are) represent insurance buyers, i.e., law firms. The primary advantage to using a broker is that they generally work with many insurers, i.e., we have access to more than 20 legal malpractice insurers, including many that don’t use a program administrator.

How long do you have to renew a life insurance policy?

Many insurers allow a grace period of sorts for up to two weeks after a policy expires, during which you can renew.

What is prior acts coverage?

Prior Acts coverage., a/k/a Retroactive coverage, covers a firm for claims arising out of work that it did prior to the inception date of its current policy (hence the name “prior acts coverage”). Without it, a firm is covered only for malpractice that it committed on or after the inception date of its current policy.

What is the Main Difference Between an Occurrence vs Claims-Made Malpractice Policy?

Occurrence malpractice insurance provides coverage for incidents that occurred during the policy year, regardless of when a claim is reported to the carrier.

What are the Costs of Occurrence vs Claims-Made Malpractice Policies?

The cost of each type of policy varies by a number of factors, including location, specialty, procedures provided, and prior claims history. Typically, claims-made policies cost less at the start of the policy, and rates rise each year as the policy matures.

Why is There a Difference in Price Between Occurrence vs Claims-Made Premiums?

Occurrence rates are more concrete, whereas claims-made rates are more fluid. Claims-made coverage allows carriers to more accurately match price to risk for the time period being covered.

Are There Differences in Coverage for Certain Types of Medical Care?

There is no difference in the type of medical care or procedures that are covered under occurrence vs claims-made malpractice policies, but not all doctors will qualify for occurrence coverage.

Are There Differences in the Limits of Coverage for Occurrence vs Claims-Made Malpractice Insurance?

It’s important to note that there are differences in how the limits of coverage are applied to occurrence vs claims-made policies. If you have a standard policy of $1 million per occurrence/ $3 million per annual aggregate with an occurrence policy, those coverage limits apply to each year of the policy.

Can I Switch Between Occurrence and Claims-Made Malpractice Policies?

It’s easier to switch from an occurrence policy to a claims-made policy than vice versa, due to the cost of tail coverage. If you have a claims-made policy with rising rates and you decide to switch to an occurrence policy, you will still need to purchase tail insurance.

Popular Posts:

- 1. how to file for divorce in florida without an attorney

- 2. how to get power of attorney in nj

- 3. how to research an attorney track record

- 4. how to choose an attorney

- 5. how to fight attorney fees

- 6. which excerpt from part one of trifles most develops the motives of the county attorney?

- 7. how to find a pro bono attorney

- 8. what type of software can your parents use to create a will without visiting an attorney?

- 9. who is my district attorney

- 10. how to get power of attorney for parent with dementia