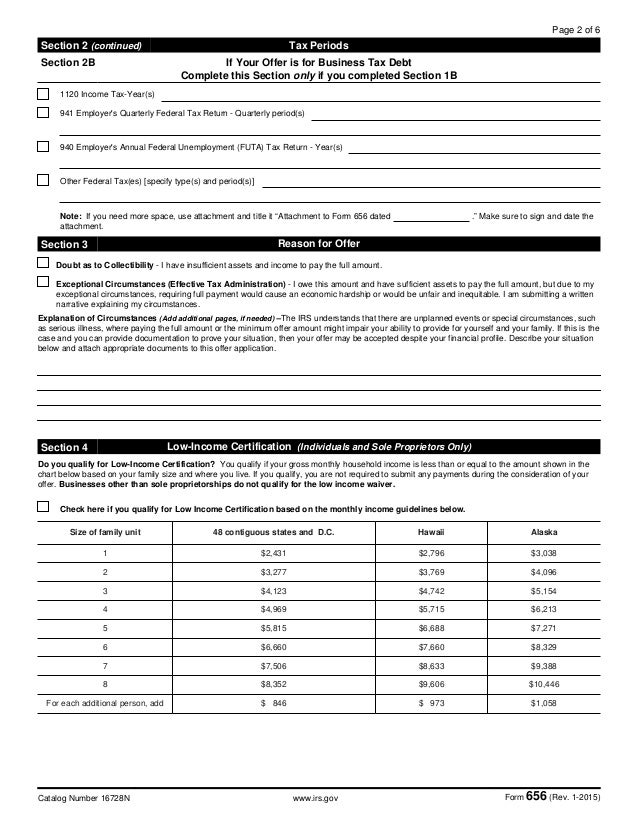

These include cases where you are alleging unlawful discrimination, such as job-related discrimination on account of race, sex, religion, age, or disability. Such attorney fees are deductible "above the line" as an adjustment to income on your Form 1040. This means you don't have to itemize your personal deductions to claim them.

Any legal fees that are related to personal issues can't be included in your itemized deductions. According to the IRS, these fees include: Fees related to nonbusiness tax issues or tax advice. Fees that you pay in connection with the determination, collection or refund of any taxes.Oct 16, 2021

Full

AnswerWhere do legal fees go on 1040?

Feb 07, 2019 · You may deduct 100% of the attorney fees you incur as a plaintiff in certain types of employment-related claims. These include cases where you are alleging unlawful discrimination, such as job-related discrimination on account of race, sex, religion, age, or disability. Such attorney fees are deductible "above the line" as an adjustment to income on …

Which legal fees can you deduct on your taxes?

Nov 27, 2018 · For example, if you had to pay attorney fees related to personal matters, you would have previously been able to deduct an amount that …

Can you deduct lawyer fees on taxes?

You may be able to deduct, as an adjustment to income on your Schedule 1 (Form 1040), attorney fees and court costs for actions settled or decided after October 22, 2004, involving a claim of unlawful discrimination, a claim against the U.S. Government, or a claim made under section 1862(b)(3)(A) of the Social Security Act.

Are my attorney fees tax deductible?

Feb 17, 2022 · It’s just one of many odd rules how legal settlement are taxed. This harsh tax rule usually means plaintiffs must figure a way to deduct …

Are legal fees tax deductible in 2019?

Key Takeaways. With a few exceptions, individual taxpayers may not deduct legal expenses on their tax returns. Exceptions include legal fees in connection with an employment discrimination lawsuit and any amounts earned in connection with whistleblower suits.

What legal expenses are deductible?

These include: Attorney fees, court costs, and similar expenses related to the production or collection of taxable income. Fees for defending against criminal charges related to trade or business (legal fees for criminal charges against an individual, such as the business owner, are not tax-deductible)Apr 16, 2021

What legal and professional fees are tax deductible?

Legal and professional fees that are necessary and directly related to running your business are deductible. These include fees charged by lawyers, accountants, bookkeepers, tax preparers, and online bookkeeping services such as Bench.Mar 8, 2022

Are attorney fees tax deductible in California?

Attorney's fees incurred as an “ordinary and necessary” expense of the business can be deducted in Schedule C, Line 17.Jun 1, 2019

Can you claim legal fees on tax return?

You can deduct any legal fees you paid in the year to collect or establish a right to collect salary or wages. You can also deduct legal fees you paid in the year to collect or establish a right to collect other amounts that must be reported in employment income even if they are not directly paid by your employer.Jan 18, 2022

Are legal fees tax deductible in 2020?

Any legal fees that are related to personal issues can't be included in your itemized deductions. According to the IRS, these fees include: Fees related to nonbusiness tax issues or tax advice. Fees that you pay in connection with the determination, collection or refund of any taxes.Oct 16, 2021

Where do legal fees go on 1040?

For 2021, Schedule 1 to Form 1040 gives you two lines. Line 24(h) and 24(i) of Part II, Adjustments to Income. Why worry about deducting legal fees in the first place? Most plaintiffs would rather have the lawyer paid separately and avoid the need for the deduction.Feb 17, 2022

Are legal fees capitalized?

However, the IRS recently finalized regulations that are effective for 2014 that clarify that legal fees must at times be capitalized as an asset for tax purposes, and thus may not be immediately deducted.

Examples of Deductible Fees

Examples of attorney fees that produce or collect taxable income and that can qualify for a tax deduction include the following: 1. Tax advice you...

Examples of Nondeductible Fees

Generally, you can't deduct fees paid for advice or help on personal matters or for things that don't produce taxable income. For example, you can'...

How to Deduct Attorney Fees

Generally, you deduct personal attorney fees as an itemized miscellaneous deduction on Schedule A of your Form 1040 tax return. This means you get...

Attorney Fees For Your Business

If you own a business and hire an attorney to help you with a business matter, the cost is deductible as a business operating expense, subject to a...

Questions For Your Attorney

1. My employer hired an attorney to defend me in a discrimination suit. I don't like the way he's handling the case. If I hire you to defend me, ca...

Are Legal Expenses Deductible?

You might be wondering, "Are attorney fees deductible?" You must first determine whether or not your specific legal expenses are, in fact, deductible. This has become a particularly relevant question following the passage of the Tax Cuts and Jobs Act, which has rendered some legal deductions void for the foreseeable future.

Eligible Legal Deductions to Explore

Keep in mind that you can still deduct legal expenses that are directly related to your business as an independent contractor. Although these fees will require extensive documentation, they can still qualify as an eligible deduction and should be incorporated into your Schedule C Form.

Can you deduct attorney fees on taxes?

In most instances, the attorney fees from these cases can't be deducted from your taxes.

Can you deduct legal fees?

Legal fees that are deductible. In general, legal fees that are related to your business, including rental properties, can be deductions. This is true even if you didn't win the legal case in which the legal fees were incurred. For instance, according to the IRS, you can deduct:

What are legal fees?

Any legal fees that are related to personal issues can't be included in your itemized deductions. According to the IRS, these fees include: 1 Fees related to nonbusiness tax issues or tax advice. 2 Fees that you pay in connection with the determination, collection or refund of any taxes. 3 Personal legal expenses, including:#N#Child custody#N#Purchasing real estate#N#Breach of promise to marry#N#Civil or criminal charges related to personal relationships#N#Personal injury#N#Title preparation#N#Estate planning such as will preparation#N#Property claims or settlements#N#Divorce 4 Fees for defending civil or criminal charges that arise from your participation in a political campaign

What are some examples of miscellaneous deductions?

For example, the following can generally no longer be included in miscellaneous deductions: 1 union dues 2 work clothes 3 hobby expenses 4 tax preparation fees 5 investment expenses

Can you deduct legal fees for rental property?

In general, legal fees that are related to your business, including rental properties, can be deductions. This is true even if you didn't win the legal case in which the legal fees were incurred. For instance, according to the IRS, you can deduct: Fees that are ordinary and necessary expenses directly related to operating your business ...

Can you take the standard deduction on taxes?

When filing your taxes, you can usually either choose to take the standard deduction or to itemize deductions. Both of these options will typically reduce your taxable income, which means that you'll pay less in taxes. In the case of deducting your legal fees, you need to itemize your deductions rather than taking the standard deduction for ...

What is the 2% rule?

This rule meant that taxpayers who couldn't write off certain expenses related to their jobs were allowed to deduct a portion of those itemized miscellaneous expenses that exceeded 2% of their Adjusted Gross Income (AGI).

Can you deduct expenses that are not deductible?

In addition to the expenses that are no longer deductible as a miscellaneous itemized deduction, there are expenses that are traditionally nondeductible under the Internal Revenue Code. Both categories of deduction are discussed next.

Can you deduct education expenses on 1040?

If you were an eligible educator for the tax year, you may be able to deduct qualified expenses you paid as an adjustment to gross income on your Schedule 1 (Form 1040), rather than as a miscellaneous itemized deduction. See the Instructions for Forms 1040 and 1040-SR for more information.

Can nonresident aliens be deducted?

Generally, nonresident aliens who fall into one of the qualified categories of employment are allowed deductions to the extent they are directly related to income which is effectively connected with the conduct of a trade or business within the United States.

How to order prior year IRS forms?

Go to IRS.gov/OrderForms to order current forms, instructions, and publications; call 800-829-3676 to order prior-year forms and instructions. The IRS will process your order for forms and publications as soon as possible.

Can you deduct unreimbursed employee expenses?

You can deduct unreimbursed employee expenses only if you qualify as an Armed Forces reservist, a qualified performing artist, a fee-basis state or local government official, or an employee with impairment-related work expenses.

What expenses can be deducted from gross income?

The amount of expenses you can deduct as an adjustment to gross income is limited to the regular federal per diem rate (for lodging, meals, and incidental expenses) and the standard mileage rate (for car expenses) plus any parking fees, ferry fees, and tolls. The balance, if any, is reported on Schedule A.

What is a fee basis official?

You are a qualifying fee-basis official if you are employed by a state or political subdivision of a state and are compensated, in whole or in part, on a fee basis.

Is a contingency fee deductible?

Typically you pay a contingency fee where the attorney recovers a percentage of any settlement or award. If the award is for physical personal injuries or sickness, then attorney’s fees are not deductible because they relate to a tax-free recovery. However, the fees related to taxable damages, such as punitive damages or any amounts related ...

Is alimony deductible in divorce?

Divorce. Generally, fees in the course of a marital dissolution are not deductible. However, fees that relate to obtaining taxable alimony may be deductible on 2017 returns as a miscellaneous itemized deduction subject to the 2%-of-AGI floor.

Is estate planning tax deductible?

Generally, fees to prepare a will or handle other estate-planning matters are not deductible. However, if an attorney can specify the portion of the fees that relate to estate tax planning, then that portion may be deductible as a miscellaneous itemized deduction (subject to the 2%-of-AGI floor) on 2017 returns.

Is marital dissolution deductible?

Generally, fees in the course of a marital dissolution are not deductible. However, fees that relate to obtaining taxable alimony may be deductible on 2017 returns as a miscellaneous itemized deduction subject to the 2%-of-AGI floor. Fees to protect one’s business or other assets during a property settlement are not deductible, even though they relate to business or the production of income.

Popular Posts:

- 1. how to file for divorce in florida without an attorney

- 2. how to get power of attorney in nj

- 3. how to research an attorney track record

- 4. how to choose an attorney

- 5. how to fight attorney fees

- 6. which excerpt from part one of trifles most develops the motives of the county attorney?

- 7. how to find a pro bono attorney

- 8. what type of software can your parents use to create a will without visiting an attorney?

- 9. who is my district attorney

- 10. how to get power of attorney for parent with dementia