Ultimately, all trust accounts should be in the name of an attorney or the firm. Trade names cannot be used on trust accounts. In deciding whether or not to use the name of an attorney or a firm, that will come down to whether or not the firm has multiple attorneys and what the name of the firm is.Sep 4, 2020

Full

AnswerWhat is an attorney trust account?

2 days ago · Instead, it will first go into the trust account so that the attorney can deduct fees, third-party claims, and expenses. Before IOLTA came about in the early 1980s, trust accounts were to be put ...

Can a lawyer hold client funds in a trust?

Attorney trust accounts are a third type of account, which may or may not be interest-bearing. For most attorneys, a non-IOLTA trust account is used for an individual client with a large balance on hold, such as a personal injury payout. If the account accrues …

Can a lawyer reconstruct a firm's Trust Account records using bank statements?

Apr 08, 2015 · At its most basic level, Trust Accounting is simply bookkeeping of trust accounts in accordance with state requirements. These requirements vary from state to state, but they have a few rules in common. Namely, there is to be no comingling of client funds with the lawyer or law firm’s funds, and maintaining accurate records is a must.

How do I contact a Trust accountant?

Sep 12, 2018 · The attorney trust account ensures the separation and security of client funds and helps law firms avoid accidently comingling client funds with law firm funds. Generally speaking, there are two guidelines law firms should abide by: 1. Maintain a single account to hold all client funds that is separate from the law firm’s operating money.

What is an attorney trust account definition?

Definition: A trust account is a special bank account that a lawyer must maintain when the lawyer receives and holds money on behalf of the lawyer's clients or third parties.Apr 29, 2015

How do I set up a trust in QuickBooks?

Here's how to create a trust account in QuickBooks Online:Click the Gear icon at the top and select Chart of Accounts.Select the New tab at the upper right corner.For Account type. Select Other Current Liabilities.Select Trust Accounts under Detail Type.Type in your desired name under Name.Click Save.Jan 30, 2019

What is the difference between an operating account and a trust account?

Operating Accounts are firm fund accounts that can receive Bill Payments. Bill Payments include matter, payroll, office expenses, etc. Whereas, a Trust Account is where the attorney holds the client's trust funds on behalf of the client for the use of paying Bills.Mar 28, 2021

What type of account is an IOLTA?

Interest on Lawyers Trust AccountsIOLTA is an acronym for Interest on Lawyers Trust Accounts. Whenever a lawyer has funds that belong to a client, state ethics rules require that those funds must be kept in a trust account that's separate from the lawyer's general operating account.

How do I set up an attorney trust in QuickBooks?

1:056:37How To Set Up Trust Accounting in QBO Advanced (WIthout LeanLaw ...YouTubeStart of suggested clipEnd of suggested clipAccount with the detail type of trust account liabilities. We'll name it for the client sampleMoreAccount with the detail type of trust account liabilities. We'll name it for the client sample client and then the key thing is making it a sub account under the funds held in trust liability.

How do you record a trust transaction?

0:544:30How to Record Trust Transactions - YouTubeYouTubeStart of suggested clipEnd of suggested clipAccount from the drop-down box and then select new transaction on the top right in this newMoreAccount from the drop-down box and then select new transaction on the top right in this new transaction window type in the amount that you are depositing into your clients trust account in the amount.

How do you create a trust account?

To prepare an accurate trust accounting, an inventory of trust property, and copies of all account statements, invoices, and receipts must be kept. It is recommended that trustees keep records organized and utilize financial planning software to better track expenses and investments.Oct 31, 2019

How do I open a trust account?

General Documentation for opening Savings Account of Trust/NGORegistration Certificate of Trust / Society / Association/ Club.Trust Deed / Bye-laws / Constitutional Document (If unregistered, notarized copy to be obtained)Copy of PAN Card.Income Tax registration u/s 12A for entities as specified in RBI circular.More items...

How do trust bank accounts work?

In a trust account, the bank acts as a custodian of the account while the trustee has legal control over the account's assets. Assets can be anything from cash, stocks, and bonds to real estate and other types of property. The trustee has the responsibility of managing the account's assets.

Why do attorneys keep two separate types of bank accounts?

Always keep law firm operating accounts separate from client funds accounts so that there is never any appearance of noncompliance with the rules. The easiest way to achieve this goal is with trust accounts that are integrated into case management software.Sep 12, 2018

Who controls IOLTA?

Financial Institutions' role regarding IOLTA is governed entirely by state law.

Is an IOLTA account checking or savings?

Regardless of which state you're in, you can't, under any circumstances, use an IOLTA account as a savings account or an operating account, even if the money you withdraw from the IOLTA has already been earned.Feb 14, 2020

What is an attorney trust account?

Attorney trust accounts are a third type of account, which may or may not be interest-bearing. For most attorneys, a non-IOLTA trust account is used for an individual client with a large balance on hold, such as a personal injury payout. If the account accrues interest, that interest goes to the client.

How to do trust accounting?

After you’ve read more about trust accounting and checked your local rules, what do you do next? Well, you can start by applying this information to how you address trust accounting in your own firm. Below are a few pointers: 1 Set clear trust accounting policies. Clearly spell out your office policies for trust accounting. This will ensure a helpful assistant does not accidentally commingle funds or commit some other clerical error. 2 Set up systems to guard against error. Do the simple stuff, like using different colored checks, to keep your name off the disciplinary list. 3 Get a little help from technology. Ditch the Excel spreadsheet or paper ledger. Use some of the many available tools to regularly track your transactions and reconcile records with bank statements. Options include Clio Manage and/or Quickbooks.

What happens when a case ends?

When a case ends, and all claims are settled, any remaining amount is refunded to the client. If there is a dispute over your fees, and you have client money in the trust account, check with your state bar—many require you to hold that money in the trust account while the fee dispute is handled.

What is a minor clerical error?

A minor clerical error or two, usually a result of sloppy office procedures, results in commingling of funds. The firm does not self-report, but does correct the error. The bar finds out later due to an unrelated ethics complaint and punishes the firm for the failure to report.

Do you have to go to a bank branch in person?

If you practice in multiple states, beware that you are in for a major headache. As far as I can tell, all banks require you to go, in person, to a branch that is physically located in the state in which you wish to open an account.

What software do lawyers use to run their own law firm?

Accounting is probably the worst part of running your own law firm. Many attorneys turn to QuickBooks or Xero for managing their accounting and recordkeeping, rather than Excel spreadsheets. QuickBooks and Xero integrate with Clio Manage, which will save time on data entry.

Can you practice law without a trust account?

In some states, you can’t even practice without having an account. Even if it’s for pro bono work. It’s common for law firms to operate one or more pooled trust accounts depending on the nature and needs of the practice. For example, firms that handle real estate matters may require several pooled trust accounts at different financial institutions. On the other hand, a criminal practice may require only one pooled trust account.

What is the role of an attorney in a trust account?

The three most common scenarios in which an attorney will be responsible for a trust account are: For funds received at the start of representation, In connection with payment from a settlement, or. When the attorney acts as a fiduciary agent on behalf of a client or a client’s estate.

What are the requirements for trust accounting?

Trust Accounting has some very specific recordkeeping requirements, which are used to maintain accurate information for both the attorney and the client. Trust Accounting requires: 1 Tracking of all deposits and disbursements made through the account. 2 A detailed ledger that notes every monetary transaction for each particular client. 3 An account journal for each account, tracking each transaction through the account. 4 Monthly reconciliation of the account.

What is trust accounting?

At its most basic level, Trust Accounting is simply bookkeeping of trust accounts in accordance with state requirements. These requirements vary from state to state, but they have a few rules in common. Namely, there is to be no comingling of client funds with the lawyer or law firm’s funds, and maintaining accurate records is a must.

Can a lawyer use a client trust account?

Lawyers should never use a client trust account to manage payroll. Again, going back to the no comingling of funds rule, there should never be a reason for a law firm’s payroll function to access a client trust. Payroll should come out of the firm’s Operating Account.

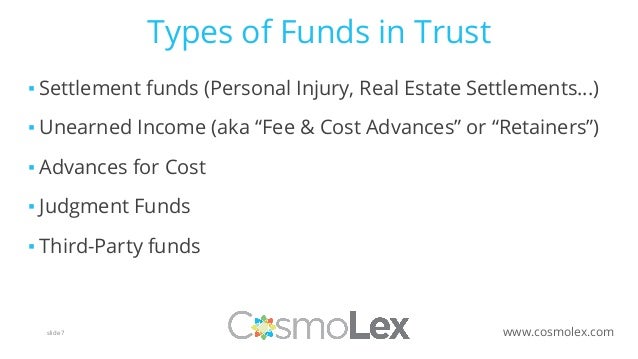

What is unearned income in a trust?

These include: Settlement Funds such as those obtained through a Personal Injury case or a Real Estate transaction. Unearned Income refers to monies paid to the lawyer or law firm before services have been rendered.

Can you track client trusts?

Keeping track of client trusts is no easy feat, especially if you manage several client trusts. Each one needs to be managed and tracked independently and must have a full paper trail so there can never be a question that funds were used improperly. Rather than rely on manual tracking or generic accounting software, more and more lawyers are turning to legal trust accounting software, like that offered by CosmoLex, to help them manage their fiduciary duties as they relate to trusts.

What are some examples of unearned income?

Fees, Cost Advances, and Retainers are all examples of unearned income. Advances for Costs are similar to unearned income, except they are to be used specifically for costs associated with managing the case. Judgment Funds, similar to settlement funds, are awarded by the court.

How to manage a trust account?

There are a lot of rules around lawyer trust accounts. To avoid trouble and remain in compliance, law firms and lawyers should consider these best practices: 1 Understand the consequences. When reviewing the rules, law firms must remain aware of the consequences of falling out of compliance with lawyer trust account rules. 2 Remain transparent. Don’t allow billing practices to become a mystery. Lawyers should leverage legal industry specific software like Smokeball to track time and expenses accurately. 3 Educate clients. Help clients understand what an attorney trust account is and what their rights are. The less ignorance there is around how a client’s retainer or other funds are being handled, the fewer billing complaints a law firm will experience. 4 Never comingle funds. Always keep law firm operating accounts separate from client funds accounts so that there is never any appearance of noncompliance with the rules. The easiest way to achieve this goal is with trust accounts that are integrated into case management software.

How does Smokeball help with trust accounts?

Smokeball can provide the trust account balance on any client within minutes no matter how many client funds accounts managed by the law firm. There are also law firm insights reports and attorney time tracking software making it easy to accurately bill for attorney work on the case and provide certifiable proof when a client inquires about the status of their money and how it is being managed. If you’re looking for attorney billing software and law practice management software in one solution see a quick demo of Smokeball and see what it can do for your firm.

Why do law firms have fiduciary duty?

Every law firm has a fiduciary duty to keep client money separated from law firm funds. For example, a lawyer can’t take a client’s retainer and use that to cover operating costs unless the money has already been earned. The attorney trust account ensures the separation and security of client funds and helps law firms avoid accidently comingling ...

What is a lawyer's responsibility?

The lawyer is responsible for keeping up with the client trust account and ensuring that funds are properly handled and that the status of each client’s funds are tracked. 2.

What is an IOLTA account?

Interest on Lawyer Trust Accounts (IOLTA) IOLTA trust account definition: IOLTAs are a method of raising money to fund civil legal services for indigent clients through the use of interest earned on lawyer trust accounts. In the United States, lawyers are allowed to place client funds in interest bearing lawyer trust accounts.

How many states have IOLTA?

While all states have an IOLTA program, only 44 states require lawyers to participate. In states with mandatory IOLTA participants, the lawyer must place client funds into an attorney trust account and cannot withdraw the money until they have earned the fee. Beyond the basic rule of depositing client funds into an attorney trust account in states ...

LegalFuel: The Practice Resource Center of The Florida Bar

Then, check out the materials and forms on LegalFuel: The Practice Resource Center website. This webpage addresses the creation of trust accounts, management, and applicable rules:

Reconcile Your Trust Account

After your Trust Account has been opened for one month, you need to make it a habit to reconcile your Trust Account. And then reconcile your Trust Account every month thereafter. Check out the Practice Resource Institute for templates, spreadsheets, and helpful information to make trust reconciliation fast and simple.

Maintain a Trustworthy Trust Account

Last, but certainly not least, check out this video about Maintaining a Trustworthy Trust Account.

Trust Account Mistakes That Lawyers Often Make

William L. Pfeifer, Jr., is a former writer for The Balance Small Business and an attorney who has written extensively on legal issues and the practice of law.

How an IOLTA Account Works

Attorneys often receive retainer fees from clients when they mutually sign a retainer agreement that outlines the terms of the attorney's representation. That money is supposed to go into the lawyer's trust account. They're then entitled to pay that money out to themselves as they complete work for the client.

Commingling Attorney Funds With Client Money

A second major mistake often arises out of a lack of understanding about how a trust account is supposed to work.

Failing to Properly Track Client Funds

The third major way that attorneys screw up their trust accounts is by failing to keep detailed records of each client's trust account transactions .

Getting Help

Some attorneys realize that their trust accounts are screwed up, but they don't know how to fix the problem. One solution is to contact a law practice management advisor. Many state bar associations now offer free law practice management advice to their members, and a number of private management advisors also offer their services for a fee.

What are the rules for trust accounts?

The rules governing attorney trust accounts are meant to preserve the public trust that money given to an attorney to be held for the client will be held inviolate. All in all, every attorney should be familiar with the trust account rules before an audit takes place. See e.g., R. 1:21-6.

How to contact Nissenbaum Law Group?

Contact the Nissenbaum Law Group to schedule an appointment at 908-686-8000 or feel free to use the following form to e-mail us. Please include as much information as you can to ensure that we are able to handle your request as quickly as possible.

Do trust accounts need to be reconciled?

Trust accounts must be subject to a rigorous three-way reconciliation. That reconciliation will pick up such items as whether disbursements from the subaccount of one client were used to pay checks issued for a different client. 2.

What is an IOLTA account?

The most unique aspect of the chart of accounts for law firms is the IOLTA or trust account. The funds in this account do not belong to the lawyer and need to be recorded on a per client basis. In order to comply with recordkeeping rules, almost all attorneys are required to have at least two bank accounts: the normal operating bank account and the IOLTA bank account. In addition, the chart of accounts should also include a Trust Liability account to show that the funds in the IOLTA bank account do not belong to the law practice. They are, instead, owed to the client until they are earned by the attorney or disbursed in other ways.

How to keep track of expenses?

The easiest way to keep track of these is to make one or several billable expense accounts, depending if your client wants to separately keep track of filing fees, postage, medical records, travel and other expenses. First, you will need to set up an income account. Then, you can make an expense that is billable and feeds into ...

Who is Brandy Derrick?

She is the founder of Legal Ease Bookkeeping, LLC, where she and her team help solo practitioners and small law firms navigate their way to understanding their books.

Can law firms enter transactions into QuickBooks Online?

By adding in these accounts, law firms will be able to easily enter transactions properly into QuickBooks Online. Most data needed for state reporting requirements, including three-way reconciliation reports, should be easily found within the balance sheet and profit and loss statement.

Do attorneys have to keep records?

The rules vary by state, but at a minimum, attorneys are required to maintain “complete records.”. The American Bar Association publishes a list of recordkeeping requirements by state. Even though your state may have its own unique rules, there are a couple of things you should include in your clients’ chart of accounts in order to easily comply ...

Popular Posts:

- 1. how to file for divorce in florida without an attorney

- 2. how to get power of attorney in nj

- 3. how to research an attorney track record

- 4. how to choose an attorney

- 5. how to fight attorney fees

- 6. which excerpt from part one of trifles most develops the motives of the county attorney?

- 7. how to find a pro bono attorney

- 8. what type of software can your parents use to create a will without visiting an attorney?

- 9. who is my district attorney

- 10. how to get power of attorney for parent with dementia