Why do attorneys get 1099?

Lawyers receive and send more Forms 1099 than most people, in part because of tax laws that single them out. Lawyers, IRS Audits, and Forms 1099. Lawyers make good audit subjects because they often handle client funds, and many also tend to have high incomes. Since 1997, most payments to lawyers must be reported on a Form 1099.

When to issue a 1099?

- Interest on a business debt to someone (excluding interest on an obligation issued by an individual) ( Form 1099-INT)

- Dividends or other distributions to a company shareholder ( Form 1099-DIV)

- Distribution from a retirement or profit plan or from an IRA or insurance contract ( Form 1099-R)

Are 1099s required for attorneys?

The tax code requires companies making payments to attorneys to report the payments to the IRS on a Form 1099. Each person engaged in business and making a payment of $600 or more for services must report it on a Form 1099.

What 1099 is used for lawyers?

Of course, the basic Form 1099 reporting rule (for lawyers and everyone else) is that each person engaged in business and making a payment of $600 or more for services must report it on a Form 1099. The rule is cumulative, so while one payment of $500 wouldn’t trigger the rule, two payments of $500 to a single payee during the year require a Form 1099 for the full $1,000.

Do you send 1099 to lawyers?

How should payments to attorneys be reported? Payments to attorneys of $600 or more will be reported on either Form 1099-MISC or Form 1099-NEC according to the following rules: Attorney fees paid in the course of your trade or business for services an attorney renders to you are reported in box 1 of Form 1099-NEC.

Do I use 1099-MISC or 1099-NEC for attorney fees?

Therefore, you must report attorneys' fees (in box 1 of Form 1099-NEC) or gross proceeds (in box 10 of Form 1099-MISC), as described earlier, to corporations that provide legal services.

Do attorneys always receive 1099?

A client who pay fees to a law firm in excess of $600 in the course of the client's trade or business is required to issue a Form 1099. In the past, however, if the law firm was a corporation then no Form 1099 was required. As of January 1, 1998 a Form 1099 will be required even though the firm is a corporation.

Do you issue 1099 for professional services?

Payments made to vendors/independent contractors of $600 or more for services such as legal and professional fees, advertising, maintenance, repairs, commissions, etc. must be reported on the new Form 1099-NEC. This includes payments made to individuals, partnerships or LLCs and, in some cases, even corporations.

Do payments to attorneys do 1099-MISC?

If the payment to that lawyer is $600 or more and made in connection with your trade or business, the payment must be reported in box 10 of IRS Form 1099-MISC. A settlement payment to the lawyer may also require an IRS Form 1099-MISC to report the payment to the claimant, even though the payment is made to the lawyer.

What is difference between 1099-MISC and 1099-NEC?

The 1099-NEC is now used to report independent contractor income. But the 1099-MISC form is still around, it's just used to report miscellaneous income such as rent or payments to an attorney. Although the 1099-MISC is still in use, contractor payments made in 2020 and beyond will be reported on the form 1099-NEC.

What does gross proceeds paid to an attorney mean?

Gross proceeds are payments that: Are made to an attorney in the course of your trade or business in connection with legal services, but not for the attorney's services, for example, as in a settlement agreement; Total $600 or more; and. Are not reportable by you in box 7.

Do I send my accountant a 1099?

If the accountant is part of a corporation, you do not need to file a 1099. However, if the accountant is not part of a corporation, you might need to file a 1099. This includes accountants that are classified as a partnership or are independent contractors.

How do lawyers pay taxes?

Earlier, lawyers needed to file under ITR-4, but now lawyers can file under ITR-4 (Sugam) if they opt to file under presumptive taxation. They can file under ITR-4 (which is renamed as ITR-3 from FY 16-17), if they opt for normal provisions. If not, tax audit is applicable to them.

How do I fill out a 1099 form?

5:5910:24How to fill out an IRS 1099-MISC Tax Form - YouTubeYouTubeStart of suggested clipEnd of suggested clipYour Impa your employer identification number the or if. That's most cases you would leave thatMoreYour Impa your employer identification number the or if. That's most cases you would leave that blank and you'd put your social security number here. Instead total number of forms. Return.

What is Box 4 for state taxes?

This is the same as Box 4, only for money withheld toward the payee’s state tax responsibility. It includes two lines for situations where the contractor did work for your company in two different states and you withheld state tax in each.

How many places are on a 1099 NEC?

Your 1099-NEC form includes 15 places to enter information. Frustratingly, only seven of them are numbered, you don’t have to enter information on all of them, and some of them don’t apply to the 1099-NEC specifically. It’s cheaper for the IRS to make one general form and change just the letter designation than to design each form individually.

What is a 1099 NEC?

Its original version reads, “Payer made direct sales totaling $5,000 or more of consumer products to the recipient for resale.” This refers to relationships between a vendor and a retailer.

Where is the checkbox on a 1099?

This checkbox sits near the center, on the left-hand side of the central dividing line on your 1099 form. FATCA stands for Foreign Account Tax Compliance Act. It only applies to 1099-INT income in situations with significant balances in foreign bank accounts.

How much is the penalty for not filing 1099?

In general, the IRS does not like to be ignored. If they say something is due, it’s due. However, most penalties for non-intentional failures to file timely are small. Your liability is based on how many days late you are in filing the form. For example, if you are more than 30 days past the due date for filing your 1099-NEC with the IRS in a calendar year, you will be fined $50 per form. If you file your tax return or after August 1, 2020, you will be fined $270 per form.

What is the most common 1099?

Multiple types of Form 1099s exist; however, two of the most common are Form 1099-MISC information returns and, starting for the 2020 tax year, Form 1099-NEC. Small businesses, independent contractors, and other self-employed individuals must understand the new Form 1099-NEC filing rules to satisfy their tax reporting responsibility.

How much is a 1099-NEC fine?

For example, if you know that a Form 1099-NEC is required and you intentionally fail to file the form, the IRS may fine you $550 per form, which is hefty if you intentionally failed to file several 1099 forms.

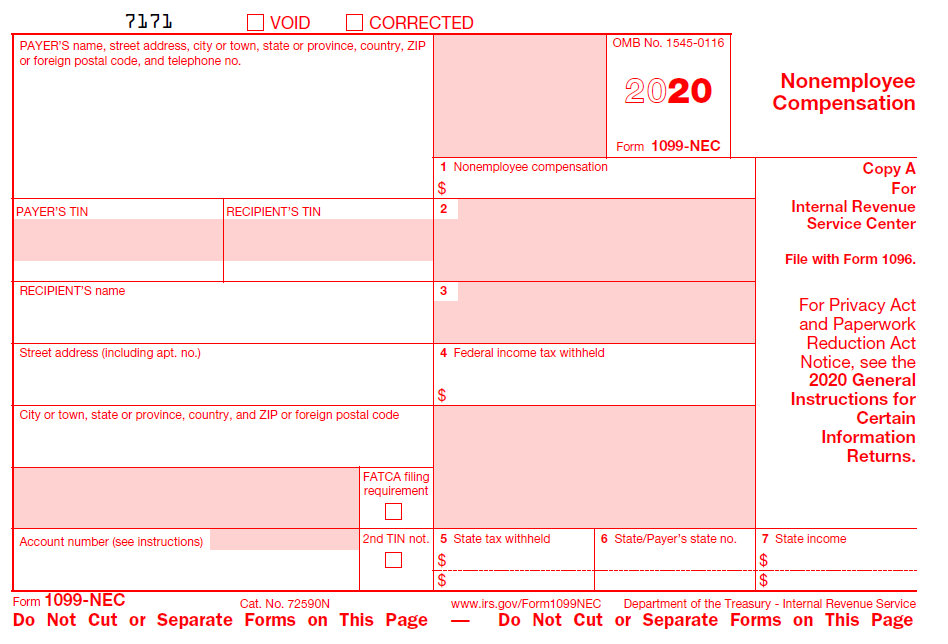

What box is non-employee compensation on 1099?

By reporting non-employee compensation in Box 1 of the 1099-NEC, the IRS is tipped off that the recipient of those fees reported may be a self-employed individual, thus subject to self-employment tax in addition to federal and/or state income tax. Self-employed individuals pay 100% of self-employment tax, where W-2 employees pay half, ...

What is an attorney 1099?

Under IRS guidance, the term “ attorney " includes a law firm or any other legal services provider on behalf of your business or trade. Remember, that 1099-NECs is for services that contribute to your business, not your personal affairs.

Is there an exception to filing 1099s?

Like any law or regulation, the 1099 legal fees rules, reporting requirements, and tax treatment change from time to time. This year is no exception. Beginning with the 2020 tax year, the Internal Revenue Service (“IRS”) has changed how taxpayers report attorney's fees. Here are four things you need to know about reporting legal fees on 1099s ...

Where are attorney payments reported on a 1099?

Certain attorney and law firm payments are reported in Box 10 of the Form 1099-MISC, not the Form 1099-NEC, if:

What is the IRS 1096?

The IRS uses Form 1096 to track every physical 1099 you are filing for the year.

What is a 1099 form?

A 1099 is an “information filing form”, used to report non-salary income to the IRS for federal tax purposes. There are 20 variants of 1099s, but the most popular is the 1099-NEC. If you paid an independent contractor more than $600 in a financial year, you’ll need to complete a 1099-NEC.

How to get a TCC for fire?

Before using FIRE, you need a Transmitter Control Code (TCC). You can request a TCC by filling out Form 4419 and then mailing or faxing it to the IRS. This form must be submitted at least 30 days before the tax deadline for your Form 1099-NEC.

How many copies of 1099 are there?

How to file a 1099 form. There are two copies of Form 1099: Copy A and Copy B. If you hire an independent contractor, you must report what you pay them on Copy A, and submit it to the IRS. You must report the same information on Copy B, and send it to the contractor.

How to obtain consent from a contractor?

Consent should be obtained in a way that proves the contractor can receive the form electronically. If you’re planning to email them a copy, you should contact them via email to obtain consent.

How to tell if a contractor is incorporated?

You can see whether a contractor is incorporated based on the information on their Form W-9. Request one from any contractor as soon as you hire them. Also keep in mind that corporation names are typically appended with “, inc.”

What to do if you don't receive a 1099-NEC?

But if you don’t receive a copy of the 1099-NEC from your client, you should follow up with them. Independent contractors will need to report all their income on Schedule C, even if it falls under the $600 range and there wouldn’t show up on any 1099s.

What if the lawyer is beyond merely receiving the money and dividing the lawyer’s and client’s shares?

What if the lawyer is beyond merely receiving the money and dividing the lawyer’s and client’s shares? Under IRS regulations, if lawyers take on too big a role and exercise management and oversight of client monies, they become “payors” and as such are required to issue Forms 1099 when they disburse funds.

Why do lawyers send 1099s?

Copies go to state tax authorities, which are useful in collecting state tax revenues. Lawyers receive and send more Forms 1099 than most people, in part due to tax laws that single them out. Lawyers make good audit subjects because they often handle client funds. They also tend to have significant income.

What is the exception to the IRS 1099 rule?

Payments made to a corporation for services are generally exempt; however, an exception applies to payments for legal services. Put another way, the rule that payments to lawyers must be the subject of a Form 1099 trumps the rule that payments to corporation need not be. Thus, any payment for services of $600 or more to a lawyer or law firm must be the subject of a Form 1099, and it does not matter if the law firm is a corporation, LLC, LLP, or general partnership, nor does it matter how large or small the law firm may be. A lawyer or law firm paying fees to co-counsel or a referral fee to a lawyer must issue a Form 1099 regardless of how the lawyer or law firm is organized. Plus, any client paying a law firm more than $600 in a year as part of the client’s business must issue a Form 1099. Forms 1099 are generally issued in January of the year after payment. In general, they must be dispatched to the taxpayer and IRS by the last day of January.

How does Larry Lawyer earn a contingent fee?

Example 1: Larry Lawyer earns a contingent fee by helping Cathy Client sue her bank. The settlement check is payable jointly to Larry and Cathy. If the bank doesn’t know the Larry/Cathy split, it must issue two Forms 1099 to both Larry and Cathy, each for the full amount. When Larry cuts Cathy a check for her share, he need not issue a form.

What percentage of 1099 does Larry get?

The bank will issue Larry a Form 1099 for his 40 percent. It will issue Cathy a Form 1099 for 100 percent, including the payment to Larry, even though the bank paid Larry directly. Cathy must find a way to deduct the legal fee.

What is technical danger?

An often-cited technical danger (but generally not a serious risk) is the penalty for intentional violations. A taxpayer who knows that a Form 1099 is required to be issued and nevertheless ignores that obligation is asking for trouble. The IRS can impose a penalty equal to 10 percent of the amount of the payment.

When do you get a 1099 from a law firm?

Forms 1099 are generally issued in January of the year after payment. In general, they must be dispatched to the taxpayer and IRS by the last day of January.

What is the newest 1099 form?

While there are a variety of 1099 forms, the newest one is 1099-NEC. It’s used to report payments to contractors and service providers who are not employees at your company and do not have taxes withheld. Before, these payments were reported using a 1099-MISC.

What is box 11 for resale?

Box 11 – Fish Purchased for Resale – If you are in the trade or business of purchasing fish for resale, you must report total cash payments of $600 or more paid during the year to any person who is engaged in the trade or business of catching fish.

What is box 6?

Box 6 – Medical and Health Care Payments – This includes payments made for various health care services such as injections or medications. Flexible spending accounts and employer-provided health care coverage are excluded. This mainly pertains to any payments made directly to a health care provider for services not covered by an insurance plan, but be sure to check with the IRS for specifics.

What is box 8 in a mortgage?

Box 8 – Substitute Payments in Lieu of Dividends or Interest – This is where you would enter aggregate payments of at least $10.00 of substitute payments received by a broker for a customer in lieu of dividends or tax-exempt interest as a result of a loan of a customer’s securities.

What is box 2 in a tax return?

Box 2 – Royalties – This is used to report royalty payments of $10.00 or more for oil and gas royalties as well as royalties for intangible property such as patents, copyrights, and trademarks.

What is a 1099 NEC?

The appropriate forms: Form 1099-NEC – Form 1099-MISC. The legal name of the contractor (NEC) or non-employee worker (MISC). Their business name (if it’s different from the contractor’s name). The federal tax classification of the contractor, so you will know whether you need to issue a 1099-NEC, or a 1099-MISC.

How to complete a 1099 NEC?

In order to accurately complete a 1099-NEC, or a 1099-MISC, you will need information usually found on the worker’s W-9. All non-employee workers should provide you a W-9 when starting their work with your business. Here’s what you need: 1 The appropriate forms: Form 1099-NEC – Form 1099-MISC 2 The legal name of the contractor (NEC) or non-employee worker (MISC). 3 Their business name (if it’s different from the contractor’s name). 4 The federal tax classification of the contractor, so you will know whether you need to issue a 1099-NEC, or a 1099-MISC. 5 Current and accurate mailing addresses. 6 Tax Identification Number (EIN) or Social Security number. 7 The total amount of funds paid to the contractor for the calendar year

Why is gross proceeds paid to an attorney important?

Why is the gross proceeds paid to an attorney category so important? For one thing, gross proceeds reporting for lawyers is not counted as income to the lawyer. Any payment to a lawyer is supposed to be reported, even if it’s entirely the client’s money to close a real estate deal. Case settlement proceeds count as gross proceeds, too.

What box is gross proceeds paid to an attorney?

Gross proceeds paid to an attorney for 2019 and prior years was box 14. But now, it is reported in box 10 of the new 2020 Form 1099-MISC. This box is only for reporting payments to lawyers. It turns out that there are numerous special Form 1099 rules for lawyers.

What box is 1099-MISC?

For 2020 and subsequent-year payments, your choices on Form 1099-MISC are more limited. Most payments are recorded in box 3, as other income. For lawyers settling cases, though, “gross proceeds paid to an attorney” is the most important category. Many lawyers may not see Form 1099 that arrive at their office, but they should be aware of this important box on the form, and what it means for their taxes.

When will 1099-MISC be reported?

It impacts their clients too. Up through 2019 payments, IRS Form 1099-MISC box 14 was for gross proceeds paid to an attorney. That means the payments you received in 2019 that were reported in early 2020 were on these 2019 forms. For payments in 2020, they will be reported in January of 2021 on a new version of Form 2020-MISC.

What is a 1099 NEC?

In other words, Form 1099-NEC reports a payment for services. For 2019 and prior years, putting income in box 7 of a Form 1099-MISC usually tipped the IRS off that this person should not only be paying income tax but also paying self-employment tax.

What is the most common 1099?

But let’s look at the realities and the different boxes on a Form 1099 before you decide. The most common version used is Form 1099-MISC, for miscellaneous income. But to discuss it, we also must also talk about the newest one, Form 1099-NEC. Up until 2020, if you were paying an independent contractor, you reported it on Form 1099-MISC, in box 7, for non-employee compensation.

When do you send a 1099?

Some businesses and law firms prefer to issue Forms 1099 at the time they issue checks, rather than in January of the following year. For example, if you are mailing out thousands of checks to class action recipients, you might prefer sending a single envelope that includes both check and Form 1099, rather than sending a check and later doing another mailing with a Form 1099.

Popular Posts:

- 1. how to file for divorce in florida without an attorney

- 2. how to get power of attorney in nj

- 3. how to research an attorney track record

- 4. how to choose an attorney

- 5. how to fight attorney fees

- 6. which excerpt from part one of trifles most develops the motives of the county attorney?

- 7. how to find a pro bono attorney

- 8. what type of software can your parents use to create a will without visiting an attorney?

- 9. who is my district attorney

- 10. how to get power of attorney for parent with dementia