How to File for Bankruptcy Without a Lawyer

- 1. Conduct a Means Test When filing a petition without a bankruptcy lawyer, the first step is to perform a “Means Test” to see if you meet the criteria for Chapter 7 bankruptcy. ...

- 2. Compile a Credit Report ...

- 3. Receive Mandatory Counseling ...

- 4. Complete the Bankruptcy Petition ...

- 5. File the Bankruptcy Petition ...

- 6. Meet with Your Creditors ...

- 7. Attend a Financial Management Course ...

Full Answer

Can you declare bankruptcy yourself?

Individuals can file bankruptcy without an attorney, which is called filing pro se. However, seeking the advice of a qualified attorney is strongly recommended because bankruptcy has long-term financial and legal outcomes.

How can I file bankruptcy without losing anything?

In bankruptcy, you'll protect property you need to work and live with bankruptcy exemptions. Nonexempt property—usually luxury items—is either lost in Chapter 7 or kept and paid for through the Chapter 13 repayment plan. You won't lose all of your property when you file for bankruptcy.

How do I prepare to file for bankruptcy?

Once you make the decision to file for bankruptcy, follow these 8 steps to ensure you are properly prepared.Choose a Bankruptcy Attorney. ... Get Together Your Bills or Make a List of Who You Owe. ... Stop Using Credit. ... Quit Paying Unsecured Creditors. ... Go on a Financial Diet. ... Determine Your Timeline.More items...•

How much debt should you have to file bankruptcy?

There is no minimum debt to file bankruptcy, so the amount does not matter. Examples of unsecured debts include credit card debt, cash advance (payday) loans, and medical bills. Secured debts: If you are behind on a house or car payment, this may be a very good time to file for bankruptcy.

What bankruptcy clears all debt?

Chapter 7 bankruptcyChapter 7 bankruptcy is a legal debt relief tool. If you've fallen on hard times and are struggling to keep up with your debt, filing Chapter 7 can give you a fresh start. For most, this means the bankruptcy discharge wipes out all of their debt.

What debts are not discharged in bankruptcy?

Additional Non-Dischargeable DebtsDebts from fraud.Certain debts for luxury goods or services bought 90 days before filing.Certain cash advances taken within 70 days after filing.Debts from willful and malicious acts.Debts from embezzlement, theft, or breach of fiduciary duty.More items...•

What do you lose when you file Chapter 7?

A Chapter 7 bankruptcy will generally discharge your unsecured debts, such as credit card debt, medical bills and unsecured personal loans. The court will discharge these debts at the end of the process, generally about four to six months after you start.

How much do you have to be in debt to file Chapter 7?

Again, there's no minimum or maximum amount of unsecured debt required to file Chapter 7 bankruptcy. In fact, your amount of debt doesn't affect your eligibility at all. You can file as long as you pass the means test. One thing that does matter is when you incurred your unsecured debt.

How long after getting a loan can you file bankruptcy?

Written by Attorney Jonathan Petts. If you've recently taken out a payday loan or made any substantial purchase, it's a good idea to wait at least 90 days to file your bankruptcy case.

Will I lose my car in Chapter 7?

If you file for Chapter 7 bankruptcy and local bankruptcy laws allow you to exempt all of the equity you have in your car, you can keep the vehicle—as long as you're current on your loan payments. And if the market value of a vehicle you own outright is less than the exemption amount, you're in the clear.

What are 5 types of debt that are not dischargeable in bankruptcy?

Nondischargeable debt is a type of debt that cannot be eliminated through a bankruptcy proceeding. Such debts include, but are not limited to, student loans; most federal, state, and local taxes; money borrowed on a credit card to pay those taxes; and child support and alimony.

Why do people file for bankruptcy?

Bankruptcy is meant for individuals who cannot make progress in paying down their debts. If this describes your situation, declaring bankruptcy can provide you with a fresh financial start.

Is there a better option than bankruptcy?

Bankruptcy Alternatives. Your options to avoid bankruptcy include debt management plans; debt consolidation loans and debt settlement.

How much do you have to be in debt to file Chapter 7?

Again, there's no minimum or maximum amount of unsecured debt required to file Chapter 7 bankruptcy. In fact, your amount of debt doesn't affect your eligibility at all. You can file as long as you pass the means test. One thing that does matter is when you incurred your unsecured debt.

What do you lose when you file Chapter 7?

A Chapter 7 bankruptcy will generally discharge your unsecured debts, such as credit card debt, medical bills and unsecured personal loans. The court will discharge these debts at the end of the process, generally about four to six months after you start.

What is lost in a bankruptcy?

Bankruptcy Can Wipe Out Credit Card Debt and Most Other Nonpriority Unsecured Debts. Bankruptcy is very good at erasing most nonpriority unsecured debts other than school loans. For instance, you can discharge unsecured credit card debt, medical bills, overdue utility payments, personal loans, gym contracts, and more.

What is Upsolve for bankruptcy?

3 minute read • Upsolve is a nonprofit tool that helps you file bankruptcy for free. Think TurboTax for bankruptcy. Get free education, customer support, and community. Featured in Forbes 4x and funded by institutions like Harvard University so we'll never ask you for a credit card. Explore our free tool

How long does a Chapter 7 bankruptcy last?

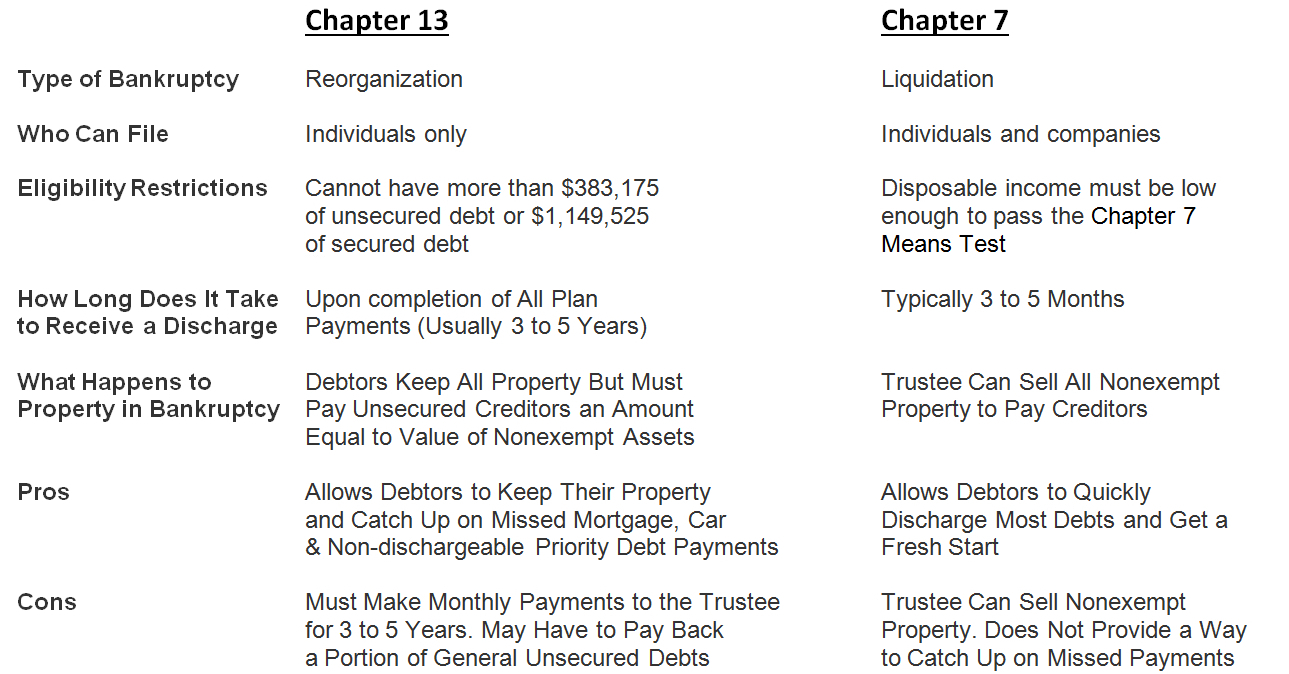

A Chapter 7 is what you think of as a traditional bankruptcy, where you walk away from your debt and get a fresh start. A Chapter 7 case lasts for a significantly shorter amount of time than a Chapter 13 case. A Chapter 13 can be much more complicated. A Chapter 13 involves a repayment plan that will run for three to five years.

What to do after 341 hearing?

After you have attended your 341 hearing and presuming there is no follow-up needed (such as filing amendments to your documents) you simply need to wait to receive your Notice of Discharge, which is the successful ending to your case. Make certain to keep a copy of this document somewhere safe.

How to determine if you qualify for Chapter 7?

First you will need to determine if you are eligible to file a Chapter 7 by passing the means test. If you are below a certain threshold for your state you will qualify, otherwise you need to complete both parts of the means test calculation to determine your disposable income.

Is Chapter 13 bankruptcy good?

A Chapter 13 case may be more beneficial to you if you have secured debt. There are also debts which are non-dischargeable in a bankruptcy case. Non-dischargeable debts include things like child support, alimony, most tax debt, etc. If the bulk of your debts are non-dischargeable a Chapter 7 bankruptcy may not offer the relief you are seeking.

How Hard Is It To File for Bankruptcy on Your Own?

You will at least need an understanding of the legal issues before filing the bankruptcy petition. How hard a case will be will also depend on other factors including :

What do you need to pay for bankruptcy?

In general, you need to at least pay a filing fee and the credit counseling and financial management course fees to finalize your bankruptcy petition. But if you have no money, you can ask for a fee waiver (in Chapter 7 cases) or ask the bankruptcy judge to roll the payment in your repayment plan (in Chapter 13 cases).

Why download bankruptcy forms?

Download the bankruptcy forms package to save the time and stress involved in tracking down the necessary materials. The packages are inexpensive and provide you with all the forms you need to file for Chapter 7 bankruptcy in your state.

What to do if you fail to report a debt?

You'll need all three reports because creditors don't typically report to every bureau. If you fail to report a debt, it won't be discharged in bankruptcy. Next, you'll have to complete a credit counseling and financial literacy course.

Do creditors have to be present at a meeting of creditors?

You'll have to attend your “ Meeting of Creditors " on the scheduled date. Although your creditors won't actually be present , the trustee will be and will ask you a number of standard questions about your case. Be sure to answer truthfully and accurately.

Do you have to fill out paperwork for bankruptcy?

Even though your case is relatively uncomplicated, a bankruptcy case requires you to fill out extensive paperwork and have a good knowledge of the Bankruptcy Code. Thus, it may be in your best interest to at least have an initial consultation with an attorney to make sure you are on the right course.

Do you need to file bankruptcy chapter?

Once you know where you’re filing and what chapter to use, it’s time to prepare your documents. At first glance, the number of documents that you need to prepare may seem overwhelming. That’s because the court requires a complete financial picture, including assets and debts, in order to process your bankruptcy. You only need to complete the forms that are applicable to your situation. However, it would be best if you went into it knowing there will be a lot of forms.

Can you fill out a bankruptcy form in Nevada?

Court personnel can’t explain how to fill out a form. They can’ t explain what the law means, tell you whether you’ve filed in the right place or give you any advice about how to accomplish your goals. Be sure to heed these warnings and take the necessary steps to proceed through your claim correctly.

Popular Posts:

- 1. how to file for divorce in florida without an attorney

- 2. how to get power of attorney in nj

- 3. how to research an attorney track record

- 4. how to choose an attorney

- 5. how to fight attorney fees

- 6. which excerpt from part one of trifles most develops the motives of the county attorney?

- 7. how to find a pro bono attorney

- 8. what type of software can your parents use to create a will without visiting an attorney?

- 9. who is my district attorney

- 10. how to get power of attorney for parent with dementia