If you’re represented by an attorney, tell the collector. The collector must communicate with your attorney, not you, unless the attorney fails to respond to the collector’s communications within a reasonable time. Consider talking to the collector at least once, even if you don’t think you owe the debt or can’t repay it immediately.

Full Answer

How to file a complaint against a debt collector?

Score: 4.6/5 (30 votes) . Collection attorneys specialize in debt collections. In addition to calling debtors and sending letters, attorneys have the power to take legal action against debtors and file a debt collection lawsuit.They have a dedicated team at their firm to handle your case who are experts in their field.

Should I pay collection agency or original creditor?

May 24, 2020 · The assumption is that you are unable to collect the debt by yourself. The first thing an attorney is going to do is ask for his fee upfront. You will be asked full details of the debt and all communication you have had with the debtor. Now you are out of pocket a few hundred dollars and your valuable time yet nothing has happened.

How to negotiate with collection agencies?

If you are a creditor, an attorney can help you put a plan in place to gain back the money you loaned out. Should you go to court, the timeframe and the amount you get will depend on the judge’s ruling. If you’re able to settle outside of court, you and the debtor will be able to …

How to handle debt collectors?

Mar 22, 2021 · You might need to hire a debt collection attorney in the following situations: You expect your case to go to court. If you've been chasing your debt for so long that you expect to require a legal judgment before you get your ... You need to send demand letters. Let's say you expect your case to go ...

How can I legally collect a debt?

But, generally, in personal matters, it's smarter to enlist the help of an attorney first. Have the attorney write a letter to the debtor....Visit our Debt Collection CenterUse a Promissory Note. ... Be Polite. ... Put Your Requests for Payment in Writing. ... Think about a Debt Settlement Agreement. ... Call in the Big Guns.

How do I write a letter for legal debt collection?

A debt collection letter should include the following information:The amount the debtor owes you.The initial due date of the payment.A new due date for the payment, whether ASAP or longer.Instructions on how to pay the debt.More items...•Mar 18, 2021

What should you not say to debt collectors?

3 Things You Should NEVER Say To A Debt CollectorNever Give Them Your Personal Information. A call from a debt collection agency will include a series of questions. ... Never Admit That The Debt Is Yours. Even if the debt is yours, don't admit that to the debt collector. ... Never Provide Bank Account Information.Sep 21, 2021

What do debt collection attorneys do?

This is conducted with a specialist lawyer's services. These services allow you and your business to legally recovery any outstanding payments, and that is done through fair, yet persistent means of communication, and if that does not materialise in the debts being settled, the case will escalate.

How long can a debt be collected?

Time limits/Statute of Limitations If your creditor does not start the court action within 6 years of the debt being due, the action can be held to be statute-barred by the court.Oct 18, 2021

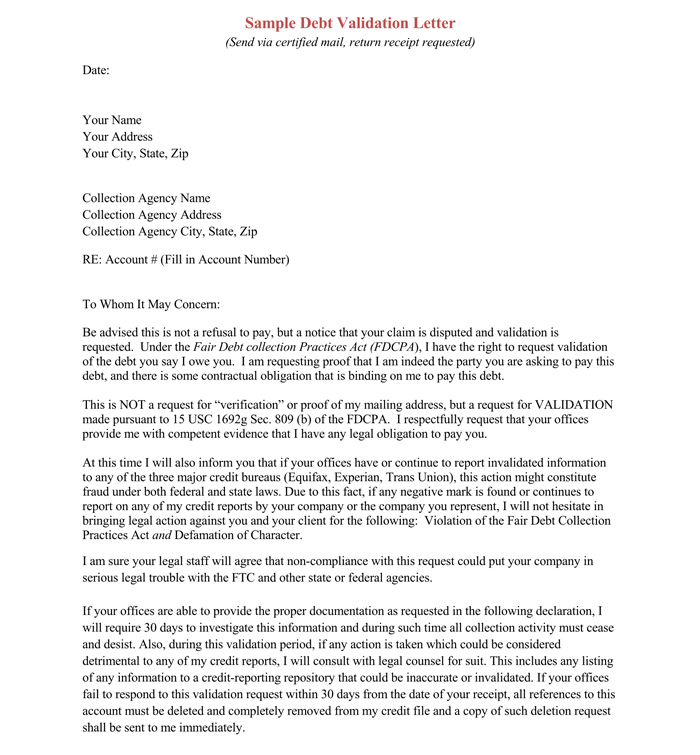

How do I dispute a debt collector letter?

The debt dispute letter should include your personal identifying information; verification of the amount of debt owed; the name of the creditor for the debt; and a request the debt not be reported to credit reporting agencies until the matter is resolved or have it removed from the report, if it already has been ...Jan 12, 2022

How do I respond to a collection letter from a lawyer?

I am responding to your contact about a debt you are attempting to collect. You contacted me by [phone/mail], on [date]. You identified the debt as [any information they gave you about the debt]. Please stop all communication with me and with this address about this debt.

How can I get out of debt without paying?

Ask for a raise at work or move to a higher-paying job, if you can. Get a side-hustle. Start to sell valuable things, like furniture or expensive jewelry, to cover the outstanding debt. Ask for assistance: Contact your lenders and creditors and ask about lowering your monthly payment, interest rate or both.Sep 2, 2021

What happens if you ignore a debt collector?

If you continue to ignore communicating with the debt collector, they will likely file a collections lawsuit against you in court. ... Once a default judgment is entered, the debt collector can garnish your wages, seize personal property, and have money taken out of your bank account.Sep 8, 2021

How can I get out of debt collectors without paying?

9 Ways to Turn the Tables on Debt CollectorsDon't Wait for Them to Call. Consider picking up the phone and calling the debt collector yourself. ... Check Them Out. ... Dump it Back in Their Lap. ... Stick to Business. ... Show Them the Money. ... Ask to Speak to a Supervisor. ... Call Their Bluff. ... Tell Them to Take a Hike.More items...•Mar 26, 2013

When should I hire a debt collector?

Most often a debt under $1000 will not result in legal action as it is not cost-effective for your business, so it is especially important to collect on those smaller debts. Once again, if the debt has gone on past 90-120 days, it is in your best interest to consider hiring a collection agency.Jun 22, 2020

Can I pay the original creditor instead of the collection agency?

Even if a debt has passed into collections, you may still be able to pay your original creditor instead of the agency. ... The creditor can reclaim the debt from the collector and you can work with them directly. However, there's no law requiring the original creditor to accept your proposal.Sep 7, 2021

Can I settle debt on my own?

Negotiating a debt settlement on your own is not easy, but it can save you time and money compared with hiring a debt settlement company. With do-it-yourself debt settlement, you negotiate directly with your creditors in an effort to settle your debt for less than you originally owed.

Is it a criminal Offence not to pay debt?

As the creditor cannot force the debtor to pay, the latter's failure to do so, despite demand, may give rise to the filing of an action to compel him to pay. ...Sep 4, 2016

Can I be chased for an old debt?

If you do not pay the debt at all, the law sets a limit on how long a debt collector can chase you. If you do not make any payment to your creditor for six years or acknowledge the debt in writing then the debt becomes 'statute barred'. This means that your creditors cannot legally pursue the debt through the courts.Dec 27, 2020

Is unpaid debt a criminal Offence?

Will you go to jail when you can't pay your credit card debt? The short answer to this question is No. The Bill of Rights (Art. ... Romel Regalado Bagares, “non-payment of debts are only civil in nature and cannot be a basis of a criminal case.Aug 3, 2020

Debt Collection Attorney

If you have used a google search to find a debt collection attorney and found our website, it is quite remarkable. These identical words appear in 1,280 URL’s, in the title of 3,490 website and in the content of 132,000,000 webpages.

Why Do You Need An Attorney?

This seems like an obvious question. “I need a debt collection attorney because I need a debt collected”. The assumption is that you are unable to collect the debt by yourself. The first thing an attorney is going to do is ask for his fee upfront.

Specialized Debt Collection Attorney

Is the attorney specialised in this field or did they have a nice advert and website? If you are searching the web there are a few guidelines that might help you.

Is A Collection Attorney Essential

You can find almost any type of users’ guides on the internet. What cannot be found is the experience a debt collection attorney will provide you in court. If you are going to end up in court – get an attorney. Do you want a different approach? Then Resolute Collections could be your answer.

Cost Of A Collection Attorney

Even the best priced collection attorney is going to set you back $125 per hour. For an experienced debt collection attorney, expect to pay $350 per hour or more. You will then have to estimate how long a defended case will take in working hours. We suggest you plan for a worst-case scenario.

Debt Settlement Negotiation

If you intend to settle your debt claim through negotiation, then we highly recommend that you engage a debt collection attorney. You are probably the worst person to negotiate a settlement if it is not a skill you use regularly. They have talents and skills which we mere mortals do not have.

Some Questions Answered

Generally not purchased. This is really up to you to find out. In our HowTo we suggest you call 3 and decide which is the best option

What does a debt collection attorney do?

A debt collection attorney can represent you if you’re a creditor or a debtor. A lawyer can help come up with strategies either to get back money that you’ve loaned out or to protect yourself from overeager creditors. Your attorney can handle paperwork for you or represent you in court.

Is Rocket Lawyer a lawyer?

This article contains general legal information and does not contain legal advice. Rocket Lawyer is not a law firm or a substitute for an attorney or law firm. The law is complex and changes often. For legal advice, please ask a lawyer.

What happens if you don't win a case?

If you don’t win, your lawyer won’t receive any payment.

What is debt settlement?

An inability to pay back loans at the present time. Threat of lawsuit from a creditor. Being treated unfairly by collectors. You may also want to consider a debt settlement attorney who can help reduce or eliminate loans in order to avoid debt collectors.

Can you settle a debt outside of court?

If you’re able to settle outside of court, you and the debtor will be able to negotiate terms. As a debtor you face the same outcomes, but instead of receiving any money, you can expect to pay back the amount you borrowed or possibly less if your attorney is able to negotiate the amount down.

What to do if you are not paying your debt?

If you need repayment for a debt and the debtor isn’t paying up, a debt collection attorney can help figure out your best course of action to get your money back. You may also want to consider a creditors rights attorney, who works solely for creditors to help them regain their money.

What is debt collection attorney?

A debt collection attorney is a lawyer who can work with you to develop legal strategies for recovering debts from nonpaying clients. Their work often involves completing and filing paperwork for you, and if your case goes to trial, they typically represent you in court.

How much does a collection agency charge?

Some collection agencies will charge 25% of your debt to work for you; some may even charge 50%. A 25% fee is probably less than what a lawyer will cost, whereas 50% is more. However, in some cases, a court judgment in your favor will require your debtor to cover your attorney fees, so your fees might not ultimately matter.

Can a lawyer be busy?

Lawyers can be quite busy, but their hectic schedules shouldn't hamper their communication with you. Surely, you'll get a feel for your potential debt collection attorney's communication process as you search for lawyers, but this initial impression only tells you so much.

Can a lawyer represent you in court?

Additionally, only attorneys can represent you in court and bring about a binding ruling from a judge. How much you actually want to go to court. If you're not invested in taking your case to court, then hiring a lawyer may not be worth it. In this case, choose a collection agency, or just leave the debt be.

Who is Max Freedman?

Max Freedman is a content writer who has written hundreds of articles about small business strategy and operations, with a focus on finance and HR topics. He's also published articles on payroll, small business funding, and content marketing. In addition to covering these business fundamentals, Max also writes about improving company culture, optimizing business social media pages, and choosing appropriate organizational structures for small businesses.

How to just say NO

Before saying no to your friend or relative, take some time, say a day or two before replying to their request. If the loan isn’t extremely urgent (e.g. a hospital emergency), it might give the borrower time to find other funding sources.

The best way to lend someone money

When you loan money to a friend, it’s important to understand that although it may help them in the short term, you are essentially providing them with a quick fix solution to what may be a long term problem.

How to collect a debt

When you have lent a friend or relative money and they are not paying you back, you’re most likely going to have to rely upon your negotiation skills to try and recover the debt. This can be tedious and depending on the nature of the relationship, can either bring you closer or can create serious tension between you.

Tips on getting your money back

Don’t fret, there are ways to deal with a friend or family member when collecting your debt!

How to collect debts?

Generally, there are three phases to the debt collection process: 1 For the first six months of your delinquency, you usually will deal with your creditor’s internal collector, which is sometimes referred to as a first-party agency (you, the debtor, are the second party). This may be an ideal time to try and settle your debt, since no middleman is involved and your lender still has an incentive to maintain a positive relationship with you. 2 Once your lender has decided that you aren’t going to repay your debt, it will be assigned to an outside organization, sometimes known as a third-party agency. At this point, the debt is still owned by, and owed to, the original creditor. If the third-party agency is successful in recovering all or part of the debt, it will earn a commission from your creditor, which can either be in the form of a fee, or a percentage of the total amount owed. 3 In the third phase of the process, your original creditor writes off your debt and sells it — often for pennies on the dollar — to an outside collection agency, sometimes known as a debt buyer. Your creditor is no longer involved. The collection agency is still trying to recoup as much of the debt as it can, in order to turn a profit on its purchase.

When was the Fair Debt Collection Practices Act passed?

The law passed Congress in 1977 as an amendment to the Consumer Credit Protection Act of 1968.

Is a collection agency still trying to recoup debt?

The collection agency is still trying to recoup as much of the debt as it can, in order to turn a profit on its purchase. In recent years, creditors have been turning over more of their delinquent accounts to debt-collection law firms, rather than to traditional bill collectors.

What does FDCPA mean?

The FDCPA: Prohibits a collection agency from discussing your debt with your family, friends, neighbors or employer. Limits the times of day collectors can call you. Prohibits the use of slurs, obscenities, insults or threats. Provides remedies for consumers who wish to stop collection agencies from all contact.

How long does it take for a debt collector to collect?

Generally, there are three phases to the debt collection process: For the first six months of your delinquency, you usually will deal with your creditor’s internal collector, which is sometimes referred to as a first-party agency (you, the debtor, are the second party).

Can debt collectors contact you?

Debt collectors are permitted to contact you by every communication system available – phone, letters, email or text message – but there are rules they must follow or they are in violation of the Fair Debt Collection Practices Act (FDCPA). Those rules include:

What a Debt Collection lawyer can do for you

If you have sued someone successfully and still are awaiting payment, you may require the services of a debt collection attorney. There are different debt collection regulations and procedures that a debt collection lawyer can use to most effectively get your money.

Why hire a Debt collection attorney

If you are part of a legal case involving debt collection, you may want to hire a debt collection attorney. A lawyer with experience in debt collection can help fight for your rights as a consumer, defending you against a debt collector or creditor.

Did you know?

According to WebRecon, a record breaking 12,000 debt collection lawsuits are expected to be filed in 2010, up from 9,300 in 2009 and 4,400 in 2007.

Popular Posts:

- 1. how to file for divorce in florida without an attorney

- 2. how to get power of attorney in nj

- 3. how to research an attorney track record

- 4. how to choose an attorney

- 5. how to fight attorney fees

- 6. which excerpt from part one of trifles most develops the motives of the county attorney?

- 7. how to find a pro bono attorney

- 8. what type of software can your parents use to create a will without visiting an attorney?

- 9. who is my district attorney

- 10. how to get power of attorney for parent with dementia