The average limits of liability purchased by small firms in California are $500,000 per claim / $1,000,000 aggregate. How do I compare policies? There is no such thing as a “standard” legal malpractice insurance policy.

Full

AnswerWhat is the minimum malpractice insurance limit?

Oct 08, 2018 · Indeed, we note on our website at the established pro-victims’ legal malpractice law firm of Glickman & Glickman in Los Angeles the estimate that only about 60% of all U.S. attorneys carry malpractice insurance. In fact, it is not even required that they do so in California, with current law holding that such coverage is voluntary.

How does legal malpractice insurance cover legal fees?

Nov 05, 2018 · The Malpractice Insurance Working Group is considering several options that may become part of the recommendations it will make to the Board of Trustees early next year, and seeks comment on these options. Options Under Consideration: Amending rules requiring attorneys to disclose to clients that they do not carry legal malpractice insurance.

How many malpractice lawsuits will insurance companies penalize a law firm?

Currently, California Rule of Professional Conduct 1.4.2 requires lawyers to inform clients in writing if they do not have professional liability insurance, with some exceptions.

What is claims-made coverage for legal malpractice?

Feb 23, 2022 · Typical limits for employed lawyers policies range from $1 million to $5 million. The limit a company will purchase depends on factors like the risk tolerance of the company, number of employed lawyers on staff, and the nature …

Do California attorneys need malpractice insurance?

Although many non-lawyers, and even some lawyers, in California believe liability insurance already is mandatory for lawyers, it is not. Rather, California's Rules of Professional Conduct merely require that any lawyer who does not have insurance disclose that fact to his or her clients.

How much does malpractice insurance cost for lawyers in California?

In general, attorneys can expect to pay between $2500 - $3500 for a comprehensive policy with commonly accepted limits. With 4-5% of practicing lawyers in the U.S. facing a legal malpractice claim in any given year, you need to know what drives the true cost of lawyers' malpractice insurance.

Do you need malpractice insurance in California?

In the state of California, physicians are not required to carry malpractice insurance. Even though malpractice insurance isn't required in California, physicians may still want to obtain this coverage. You may find that a hospital or another facility requires its visiting providers to have malpractice insurance.

How much does medical malpractice insurance cost in California?

Malpractice Insurance Rates for California DoctorsSpecialtyApproximate RateMaximum RateEmergency Medicine$23,000$38,000Family Practice No Surgery$9,000$18,000General Practice No Surgery$9,000$18,000General Surgery$30,000$60,00011 more rows•Dec 8, 2020

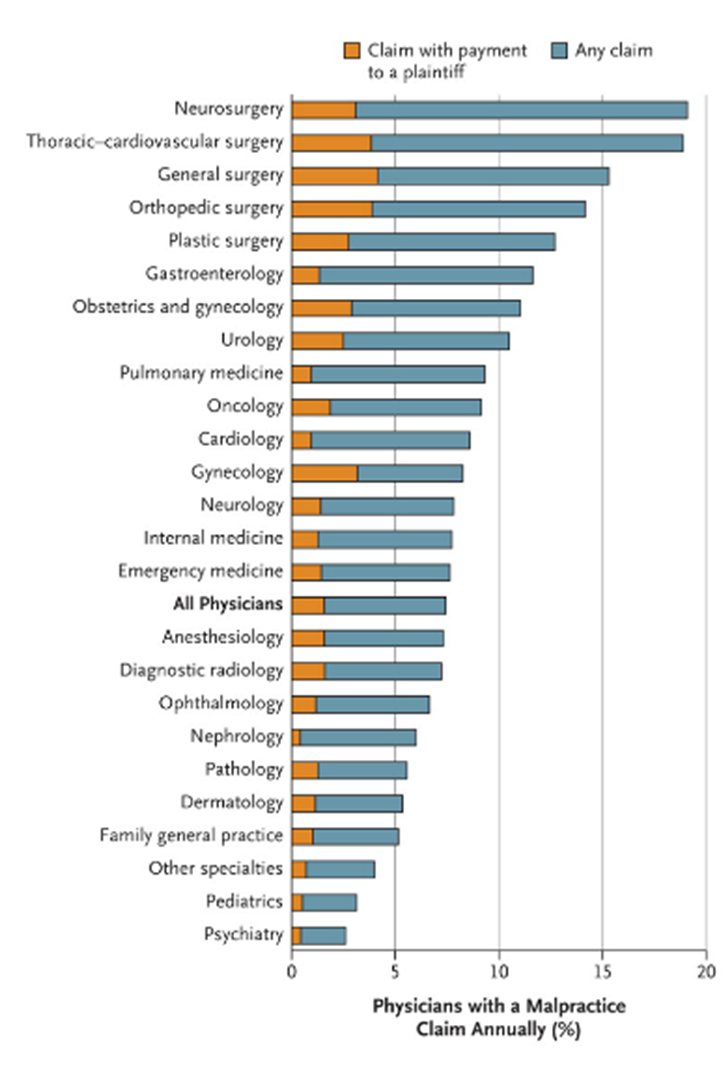

Which doctors pay the most for malpractice insurance?

Therefore, doctors in specialties that are considered higher risk pay more for their malpractice insurance. Typically, surgeons, anesthesiologists and OB/GYN physicians are charged higher premiums.

What does defense inside the limits mean?

Defense inside the limit means that all defense costs (attorney's fees, court costs, investigation and filing legal papers) are deducted first from the policy limit, which cuts into the overall limit of dollars available to pay for monetary damages awarded by a ruling.

Do doctors need professional indemnity insurance?

If a patient has suffered harm as a result of a doctor's negligence, it's important that doctors have adequate and appropriate insurance or indemnity to compensate the patient. Insurance and indemnity may also provide you with access to personal regulatory and medico-legal support and advice if you ever need it.

What is tail coverage?

Tail coverage is an addition to a claims-made policy. It extends coverage for incidents that happened during the time you had your policy, but a claim was not filed until after your policy expired or was canceled. Tail coverage is another name for an extended reporting period.

When a physician has malpractice insurance who should they contact first when faced with a malpractice lawsuit?

The first step to starting a medical malpractice case is contacting the doctor or medical professional who works with you before you actually file the claim.Jul 2, 2019

What is the best definition of malpractice?

Definition of malpractice 1 : a dereliction of professional duty or a failure to exercise an ordinary degree of professional skill or learning by one (such as a physician) rendering professional services which results in injury, loss, or damage. 2 : an injurious, negligent, or improper practice : malfeasance.

Background

The State Bar’s Board of Trustees appointed a Malpractice Insurance Working Group to conduct a statutorily-mandated review and study regarding issues related to errors and omissions insurance for attorneys, including:

Discussion

The Malpractice Insurance Working Group has researched, collected data, and taken live testimony on numerous topics related to lawyers professional liability (malpractice) insurance, including the following:

LEGAL MALPRACTICE INSURANCE COST: how much attorneys pay for their coverage, and the factors that determine the premium

Published by Lawyers Insurance Group, legal malpractice insurance brokers.

I. Legal Malpractice Insurance Cost – Fast Facts

Most sole practitioners will pay $500 – $1,000 for their first policy. A 2-atty. firm will pay slightly less than double that; a 3-atty. firm, slightly less than triple that, etc. Premiums are 25% – 50% higher in NYC, NJ, Miami-area, LA-area, and San Francisco-area; up to 35% lower in rural areas.

II. Legal Malpractice Insurance Cost – Examples of How Much Firms Pay For Their First Policy

1 Immigration $500K/$1M $2,500 $1,676#N#1 Plt. + Def Civil Lit. $1M/$1M $1,000 $2,063#N#1 Family, Crim. Def. $1M/$1M $1,000 $1,329

III. Legal Malpractice Insurance Cost – Factors That Affect Your Premium

Here are the primary factors that legal malpractice insurers use to calculate a firm’s annual premium:

There could be a negative impact on access to justice if lawyers statewide had to raise their fees to cover the costly insurance

Ed. note: Please welcome Lyle Moran to the pages of Above the Law. He’ll be writing about developments involving legal organizations in California (e.g., the State Bar of California and the new California Lawyers Association), legal issues the California Legislature takes on, as well as legal education.

Seeking DCM Associate for Hong Kong Office

Ideal candidate would have good academic credentials and some experience in leading DCM deals.

What are the exclusions on insurance?

Some typical exclusions are as follows, though many can be negotiated away or are no longer a problem on more modern forms: 1 Securities claims (some carriers will give back this coverage for additional premium) 2 Professional liability other than for legal services or professional legal liability for services taken other than at the direction of corporate counsel 3 Employment practices claims against the employer (some policies can include coverage for claims made against employed lawyers by current or former directors, officers or employees) 4 Other applicable insurance (such as D&O insurance) 5 Fines, penalties, punitive or exemplary damages 6 Trade secret misappropriation 7 ERISA (and related acts) violations 8 Bodily injury, emotional distress and property damage 9 Pollution liability 10 Prior acts, prior knowledge or prior notice of a claim or circumstance before a policy’s inception date 11 Prior and pending litigation 12 Wrongful acts committed prior to the retroactive date (including interrelated wrongful acts)

What is a 2802.A?

(a) An employer shall indemnify his or her employee for all necessary expenditures or losses incurred by the employee in direct consequence of the discharge of his or her duties, or of his or her obedience to the directions of the employer, even though unlawful, unless the employee, at the time of obeying the directions, ...

How much does malpractice insurance cost?

This means that the insurer will pay a maximum of $100,000 for defense and indemnity costs for any one claim made against your firm, and a maximum of $300,000 for all claims made against your firm during the policy year.

Who publishes legal malpractice FAQs?

Legal Malpractice FAQs is published by Lawyers Insurance Group, legal malpractice insurance brokers. Our mission is to obtain the best terms available in the market for your firm. We accomplish this by scouring the market on firms’ behalf, leveraging our access to dozens of “A”-rated legal malpractice insurers.

What are legal services?

Here’s a representative definition of “legal services”, from CNA’s policy: 1 A.”services, performed by an Insured for others as a lawyer, arbitrator, mediator, title agent or other neutral fact finder or as a notary public. 2 B. services performed by an Insured as an administrator, conservator, receiver, executor, guardian, trustee or in any other fiduciary capacity and any investment advice given in connection with such services;”

What is defense indemnity?

Defense costs and indemnity payments incurred to resolve claims filed against an attorney for acts/errors/omissions made in the course of providing legal services on behalf of the named insured, i.e., the entity (firm or individual) that bought the policy.

What is insurance broker?

Insurance brokers – brokers (which is what we are) represent insurance buyers, i.e., law firms. The primary advantage to using a broker is that they generally work with many insurers, i.e., we have access to more than 20 legal malpractice insurers, including many that don’t use a program administrator.

How long do you have to renew a life insurance policy?

Many insurers allow a grace period of sorts for up to two weeks after a policy expires, during which you can renew.

What is prior acts coverage?

Prior Acts coverage., a/k/a Retroactive coverage, covers a firm for claims arising out of work that it did prior to the inception date of its current policy (hence the name “prior acts coverage”). Without it, a firm is covered only for malpractice that it committed on or after the inception date of its current policy.

How many hours do solo attorneys work?

Typically a solo attorney will not come across this pricing factor as most solo attorneys work at least 40 hours a week. But, for attorneys working part time, they can experience a pricing discount for the annual hours worked. Some insurance programs do not offer part time policies, especially for solo attorney firms.

How much is a deductible on a car insurance policy?

Most policies require the firm to carry a deductible. The lowest available deductible is usually $1,000. Other common deductibles are $2,500 and $5,000. However, if you want to save on premium, you can have a deductible of $10,000 or higher.

What is step rate insurance?

Step rate is an industry wide pricing structure where the cost of insurance gradually increases during the first few years of coverage. Professional liability insurance is most commonly provided on a claims made policy. Because of this, your first year of coverage will be the least expensive year. The cost of insurance increases each year ...

What is claim history?

Claim History. Claim history is another factor insurance companies consider when determining the cost of professional liability insurance. Insurance carriers recognize that all claims are not created equal. If a claim is reported but nothing is paid out, you can expect little to no change to your premium.

What is considered consideration?

A consideration is the nature and extent of both your business and personal assets, since, if you are liable for malpractice, your personal assets are potentially subject to collection under a judgment. Another consideration in determining your appropriate limit is whether you want a per claim limit for a given policy period for multiple claims. ...

What are high risk areas?

Some of the higher risk areas may include transactions involving securities, intellectual property, trusts and estates, plaintiff’s personal injury cases, and newly emerging areas such as loan modifications. In the intellectual property area, most carriers consider patent work a high risk area of practice, but, ...

Does in house counsel cover moonlighting?

This coverage is generally called “Employed Lawyers Coverage” and may or may not cover moonlighting and/or pro bono work.

I. Legal Malpractice Insurance Cost – Fast Facts

- Most sole practitioners will pay $500 – $1,000 for their first policy. A 2-atty. firm will pay slightly less than double that; a 3-atty. firm, slightly less than triple that, etc. Premiums are 25%...

- The premium is based mainly on your firm’s atty. count, practice areas, policy limits, and county/state.

- Most sole practitioners will pay $500 – $1,000 for their first policy. A 2-atty. firm will pay slightly less than double that; a 3-atty. firm, slightly less than triple that, etc. Premiums are 25%...

- The premium is based mainly on your firm’s atty. count, practice areas, policy limits, and county/state.

- Criminal defense lawyers pay the least, then immigration; family and business; bankruptcy and employment; PI, real estate, and trusts-estates, and patent, securities, and class action lawyers, who...

- The minimum policy limits are $100,000 per claim/$300,000 annual aggregate, followed by $250,000/$500,000, which costs about 35% more, and then $500,000/$1,000,000, $1,000,000…

III. Legal Malpractice Insurance Cost – Factors That Affect Your Premium

- Here are the primary factors that legal malpractice insurers use to calculate a firm’s annual premium: Firm size– the number of lawyers in a firm, and whether each one works full-time or part-time. Note: all of the placements shown above are for full-time attorneys, which most insurers define as working more than 26 hours/week. Part-time attorneys generally pay lower pr…

IV. Legal Malpractice Insurance Cost – Learn More Or Request Quotes

- To learn more about legal malpractice insurance, visit these pages: Legal Malpractice Insurance FAQs – Coverage, Limits, Cost, etc. Legal Malpractice Insurance Policy Legal Malpractice Insurers

- If you have any questions, contact our principal broker, Curt Cooper at (202) 802-6415 or ccooper “at” lawyersinsurer.com.

- To learn more about legal malpractice insurance, visit these pages: Legal Malpractice Insurance FAQs – Coverage, Limits, Cost, etc. Legal Malpractice Insurance Policy Legal Malpractice Insurers

- If you have any questions, contact our principal broker, Curt Cooper at (202) 802-6415 or ccooper “at” lawyersinsurer.com.

- To get the best terms on your firm’s malpractice insurance, fill out our on-line application, or download, complete, and return our one-page premium estimate form: Online: Family Law Online Applica...

Further Reading

- Understanding Your Legal Malpractice Insurance Policy Part I: Claims-Made v Occurrence Coverage

- Understanding Your Legal Malpractice Insurance Policy, Part II: Claims-Made Policy Coverage Triggers

- Understanding Your Legal Malpractice Insurance Policy, Part III: Claims-Made Policy Coverage Gaps

- Understanding Your Legal Malpractice Insurance Policy, Part IV: Avoiding Claims-Made Policy Coverage Gaps

Popular Posts:

- 1. how to file for divorce in florida without an attorney

- 2. how to get power of attorney in nj

- 3. how to research an attorney track record

- 4. how to choose an attorney

- 5. how to fight attorney fees

- 6. which excerpt from part one of trifles most develops the motives of the county attorney?

- 7. how to find a pro bono attorney

- 8. what type of software can your parents use to create a will without visiting an attorney?

- 9. who is my district attorney

- 10. how to get power of attorney for parent with dementia