A financial lawyer is a specific type of lawyer who assists people with regards to legal issues related to finances. This can span a whole range of different subjects, including financial plans, financial responsibility laws, and even financial power of attorney arrangements.

A financial services lawyer is an attorney who helps people with financial legal issues. This kind of lawyer often specialize in a certain type of finance law. A financial lawyer can help clients with a wide variety of financial matters. Finance law includes many different specific areas of law.Nov 25, 2020

Full

AnswerHow to become a finance lawyer?

You may want to give your agent authority to do some or all of the following: use your assets to pay your everyday expenses and those of your family buy, sell, maintain, pay taxes on, and mortgage real estate and other property collect Social Security, Medicare, or other government benefits invest ...

What does a financial lawyer do?

A financial lawyer is a specific type of lawyer who assists people with regards to legal issues related to finances. This can span a whole range of different subjects, including financial plans, financial responsibility laws, and even financial power of attorney arrangements.

What does securities lawyer do?

The Financial Attorneys: We are a boutique law firm providing professional and profitable legal services to commercial clients. The firm is dedicated to the practice of the areas of law that belong to a commercial entity, such as: – Real estate development and financing. – Tax planning. – Corporate franchise. – Labor Relations. – Money collection.

What is the difference between finance and banking?

Dec 14, 2016 · Here are a few things to do: Gather all paperwork related to your debts. If you’re contacted by creditors or collectors, keep a log of the contacts,... Contact an attorney to go over you case. You might not think you have grounds to defend yourself, but an attorney... Let the attorney you’re ...

When A Financial Power of Attorney Takes Effect

A financial power of attorney can be drafted so that it goes into effect as soon as you sign it. (Many spouses have active financial powers of atto...

Making A Financial Power of Attorney

To create a legally valid durable power of attorney, all you need to do is properly complete and sign a fill-in-the-blanks form that's a few pages...

When A Financial Power of Attorney Ends

Your durable power of attorney automatically ends at your death. That means that you can't give your agent authority to handle things after your de...

When does a financial power of attorney take effect?

When a Financial Power of Attorney Takes Effect. A financial power of attorney can be drafted so that it goes into effect as soon as you sign it. (Many spouses have active financial powers of attorney for each other in case something happens to one of them -- or for when one spouse is out of town.) You should specify that you want your power ...

What do you do with your money?

buy, sell, maintain, pay taxes on, and mortgage real estate and other property. collect Social Security, Medicare, or other government benefits. invest your money in stocks, bonds, and mutual funds. handle transactions with banks and other financial institutions. buy and sell insurance policies and annuities for you.

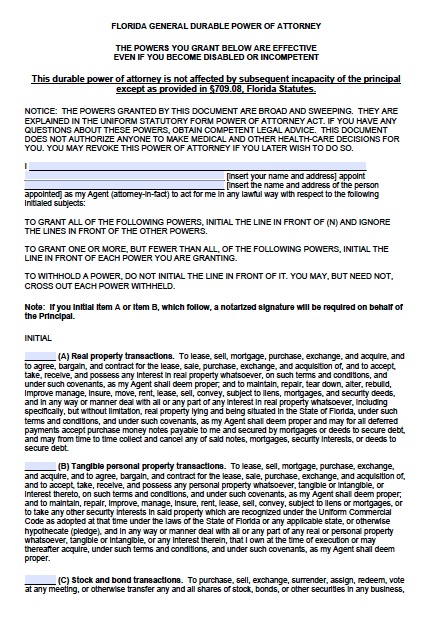

What is a durable power of attorney?

A durable power of attorney for finances -- or financial power of attorney -- is a simple, inexpensive, and reliable way to arrange for someone to manage your finances if you become incapacitated (unable to make decisions for yourself).

What happens if you don't have a power of attorney?

If you don't, in most states, it will automatically end if you later become incapacitated. Or, you can specify that the power of attorney does not go into effect unless a doctor certifies that you have become incapacitated. This is called a "springing" durable power of attorney. It allows you to keep control over your affairs unless ...

When does a power of attorney end?

When a Financial Power of Attorney Ends. Your durable power of attorney automatically ends at your death. That means that you can't give your agent authority to handle things after your death, such as paying your debts, making funeral or burial arrangements, or transferring your property to the people who inherit it.

Where do you put a copy of a power of attorney?

If your agent will have authority to deal with your real estate, you must put a copy of the document on file at the local land records office. (In two states, North and South Carolina, you must record your power of attorney at the land records office for it to be durable.)

Can you revoke a power of attorney?

As long as you are mentally competent, you can revoke a durable power of attorney at any time. You get a divorce. In a handful of states, if your spouse is your agent and you divorce, your ex-spouse's authority is automatically terminated. In other states, if you want to end your ex-spouse's authority, you have to revoke your existing power ...

What is a financial power of attorney?

A financial power of attorney is just a document you need when you want to grant someone else the power to make money decisions for you. And it’s usually created alongside your will. This kind of POA is written specifically to let someone else act as your legal rep for financial matters. Much like other powers of attorney, ...

What is a financial POA?

Just as a medical POA only applies to medical choices someone makes for you, the financial POA extends no further than the right for someone else to make money decisions if and when you’re unavailable to do so yourself. (In case you’re wondering, you need both kinds of POA to have full protection.)

What is a POA in financial planning?

With a financial POA, your agent can keep everything moving smoothly with your money. Like most legal docs, the main purpose for creating a financial POA is to protect you and your family from a preventable legal battle.

Do you need a witness for a POA?

In some situations, the document may also require a witness at the time of signature. And in some states, the agent must sign to indicate they accept the assignment. In general, filling out your state’s official form is a good start to making a financial POA.

Can you name a child as a power of attorney?

If you’d like to name one of your children or someone more distantly related to serve as your agent, creating a springing power of attorney is a great option. The event that would most often trigger a financial POA into action is if the principal became incapacitated.

What is financial lawyer?

What is a Financial Lawyer? A financial lawyer is a specific type of lawyer who assists people with regards to legal issues related to finances. This can span a whole range of different subjects, including financial plans, financial responsibility laws, and even financial power of attorney arrangements. Most people generally do not have the ...

What is the role of a lawyer in financial management?

Other financial mechanisms like bonds and trusts may also require the expertise of a lawyer, who can help determine how they are managed. They can help draft legal documents to help with the management of the funds and finances.

What is financial affidavit?

Creating a financial affidavit for divorce purposes; Cases involving financial exploitation of the elderly (the elderly are often the targets of various financial scams and fraud schemes); Cases where legal penalties involve financial consequences for the defendant, such as financial penalties for drunk driving cases;

What can an attorney do?

An attorney can help you draft, review, and file documents, and can explain your legal rights at crucial steps along the way. Then, if a financial dispute or legal conflict does arise, your attorney will be familiar with your financial background and can provide legal representation in a much more effective way.

What is the most common issue in finance?

For instance, one of the most common issues connected with finances is that of financial fraud. Various people can be involved in financial fraud, including financial advisors, accountants, and other professionals. A financial lawyer can help determine: Whether a financial violation has occurred; Which parties might be held liable;

What is a lawsuit involving false statements?

Lawsuits involving false statements to deceive a financial institution (for instance, if a person has submitted false information in a loan application); Various legal matters involving financial privacy. This can involve matters ranging from credit card information to online spending habits and other data.

Is there a specific category for financial matters?

There is not always one specific category for financial matters and disputes. As mentioned, financial matters are often embedded in a wide range of legal affairs. While there are many specific financial laws and rules, these often exist in the context of the corporate world, where companies have their own lawyers on hand to manage their business issues.

What do debt attorneys do in bankruptcy?

With a bankruptcy, a debt attorney will help you prepare all the required paperwork you need in your case. They can answer your questions and give you a basic rundown on rules and procedures in the courtroom.

Why do people need debt lawyers?

Those people are seeking help from debt lawyers to fight back against aggressive debt collectors in court. If a debt collector is relentless in trying to recover money you owe, a debt lawyer is a good resource to help you understand your rights and provide a path to escape harassment or illegal tactics.

What does it mean when a creditor threatens you?

A creditor is threatening you with a lawsuit or has filed suit. Debt collectors are treating you in a way that you feel is abusive. Your creditor has repossessed your car and might be threatening you with a collection suit.

What do nonprofit agencies do?

The nonprofit agencies will cover over your expenses and income and offer advice on what the best solution is for your situation. However, if your debt problems have grown severe or you’re being threatened with legal action, it might be time to find a bankruptcy attorney.

Why are debt lawyers so popular?

Debt lawyers have become more prominent because household debt in the U.S. has jumped 11% over the last decade to an average of $134,643 (including mortgages) and credit card and auto loan debt are going over the $1 trillion, mark.

What happens if you don't pay a judgment?

If you don’t do either – and that is what happens in most cases – the creditor obtain a legal judgment against you and can pursue that until you finish paying it. Before deciding whether to hire a lawyer, defend yourself or let the creditor collect on a judgment, review the situation.

What is debt lawyer?

A debt lawyer is someone with the knowledge, credentials and skill to help consumers struggling with debt sort through their financial troubles. Representing clients in cases against debt collectors is a form of consumer law, the branch dedicated to protecting consumers against unfair trade and credit practices.

What are the duties of an attorney?

Attorneys' responsibilities can cover a wide range of duties, and they might vary somewhat depending upon the area of law in which they practice. Some common duties include: 1 Advise clients regarding ongoing litigation or to explain legal issues they might be facing or have concerns about. 2 Research the details and evidence involved in cases, such as police reports, accident reports, or pleadings previously filed in a case, as well as applicable law. 3 Interpret case law and decisions handed down by other applicable courts. This can involve analyzing the effects of a good many factors that might have been involved in other cases. 4 Develop case strategies, such as trying to resolve cases early and cost-effectively for his clients rather than go to trial. 5 Prepare pleadings and other documents, such as contracts, deeds, and wills. 6 Appear in court before a judge or jury to orally defend a client's rights and best interests.

What are the duties of a lawyer?

Some common duties include: Advise clients regarding ongoing litigation or to explain legal issues they might be facing or have concerns about. Research the details and evidence involved in cases, such as police reports, accident reports, or pleadings previously filed in a case, as well as applicable law. Interpret case law and decisions handed ...

What is an attorney?

An attorney, also called a lawyer, advises clients and represents them and their legal rights in both criminal and civil cases. This can begin with imparting advice, then proceed with preparing documents and pleadings and sometimes, ultimately, appearing in court to advocate on behalf of clients.

How many hours do lawyers work?

The majority of lawyers work full time, and many work more than 40-hour weeks, particularly those employed by large law firms or who work in private practice.

Do attorneys have to be admitted to the bar?

Some also write for their school's law journal. Admittance to the Bar: Attorneys must be admitted to the bar association of the state in which they want to practice. This requires "passing the bar," a written examination that includes taking a written ethics exam as well in some states.

Is estate law a high pressure job?

This is less common in some fields, however, such as estate law. Some specialties involve much more in the way of client/attorney interaction and meetings. This can be a very high-pressure career, with clients ' lives and livelihoods hanging in the balance.

Do criminal lawyers travel to prison?

An attorney must sometimes travel to meet with clients and, depending on his specialty, appear in court for trials, conferences, and mediation. Criminal lawyers spend a portion of their time in prisons when their clients are incarcerated. This is less common in some fields, however, such as estate law.

What is a financial power of attorney?

A financial power of attorney gives your agent the authority to make financial decisions on your behalf if you are incapacitated. In some cases, people choose the same person to serve as the agent for both medical and financial decisions. In others, people choose different people to serve in these roles.

How to become a financial agent?

Your financial agent might be able to make the following decisions for you: 1 Access your accounts to pay your bills 2 File your tax returns 3 Make investment decisions for you 4 Collect debts that are owed to you 5 Manage your property 6 Apply for public benefits for you

What is a power of attorney?

A power of attorney document allows you to choose a trusted person who will act on your behalf if you ever become incapacitated and are unable to make decisions for yourself. The person that you choose to have the power to make these decisions is called an agent or an attorney-in-fact, but the person does not have to be a lawyer. ...

What are the two types of powers of attorney?

The two types of powers of attorney are medical powers of attorney and financial powers of attorney. A medical power of attorney allows you to choose a trusted family member or friend to make medical decisions on your behalf if you are incapacitated. A financial power of attorney gives your agent the authority to make financial decisions on your ...

What can an agent do?

What an agent can do. The powers that your appointed agent might have will depend on how your documents are written. Your health care agent might be able to make the following decisions: What types of medical care you will receive. The doctors you will see. Where you will live.

When are powers of attorney valid?

Powers of attorney are valid once they are signed; Any compensation for decision makers must be explicitly detailed in the POA document; Third parties may not be held to be liable for upholding an agent’s decision who has a POA document that looks legitimate; and. A POA designation as an agent ends when you die.

What is estate planning attorney?

Estate planning attorneys, also referred to as estate law attorneys or probate attorneys, are experienced and licensed law professionals with a thorough understanding of the state and federal laws that affect how your estate will be inventoried, valued, dispersed, and taxed after your death.

Can an estate planning attorney help with probate?

In fact, a good estate planning attorney may be able to help you avoid probate court altogether, but that largely depends on the type of assets in the deceased's estate and how they are legally allowed to be transferred.

What is a power of attorney?

At its most basic, a power of attorney is a document that allows someone to act on another person’s behalf. The person allowing someone to manage their affairs is known as the principal, while the person acting on their behalf is the agent.

Why do you need a power of attorney for an elderly parent?

Common Reasons to Seek Power of Attorney for Elderly Parents. Financial Difficulties: A POA allows you to pay the bills and manage the finances for parents who are having difficulty staying on top of their financial obligations.

What are the different types of power of attorney?

The four types of power of attorney are limited, general, durable and springing durable. Limited and general POAs end when the principal becomes incapacitated, so they’re not often used by older adults when planning for the end of life. A durable POA lasts even after a person becomes incapacitated, so is more commonly used by seniors.

How many witnesses do you need to sign a letter of attorney?

A notary public or attorney must witness your loved one signing the letter of attorney, and in some states, you’ll need two witnesses. The chosen agent must be over 18 and fully competent, meaning they understand the implications of their decision. When filling out the form, the parent must specify exactly which powers are transferring to the agent.

What are the drawbacks of a power of attorney?

The biggest drawback to a power of attorney is that an agent may act in a way that the principal would disapprove of. This may be unintentional if they are ignorant of the principal’s wishes, or it may be intentional because they’re acting in bad faith.

Is a power of attorney necessary for a trust?

Under a few circumstances, a power of attorney isn’t necessary. For example, if all of a person’s assets and income are also in his spouse’s name — as in the case of a joint bank account, a deed, or a joint brokerage account — a power of attorney might not be necessary. Many people might also have a living trust that appoints a trusted person (such as an adult child, other relative, or family friend) to act as trustee, and in which they have placed all their assets and income. (Unlike a power of attorney, a revocable living trust avoids probate if the person dies.) But even if spouses have joint accounts and property titles, or a living trust, a durable power of attorney is still a good idea. That’s because there may be assets or income that were left out of the joint accounts or trust, or that came to one of the spouses later. A power of attorney can provide for the agent — who can be the same person as the living trust’s trustee — to handle these matters whenever they arise.

Is a POA a financial responsibility?

Understand the Financial Implications of Becoming a POA. A power of attorney does not become personally liable for any of the principal’s debts or bills. However, that doesn’t mean there are no financial implications to being a POA.

Popular Posts:

- 1. how to file for divorce in florida without an attorney

- 2. how to get power of attorney in nj

- 3. how to research an attorney track record

- 4. how to choose an attorney

- 5. how to fight attorney fees

- 6. which excerpt from part one of trifles most develops the motives of the county attorney?

- 7. how to find a pro bono attorney

- 8. what type of software can your parents use to create a will without visiting an attorney?

- 9. who is my district attorney

- 10. how to get power of attorney for parent with dementia